Brexit: Four companies to invest in after the EU referendum

IBTimes UK financial expert Edmund Shing recommends firms to put your cash into post-Brexit.

The vote by the UK people to leave the European Union was clearly not anticipated by the financial markets, given the harsh reaction on Friday morning and then again on the following Monday.

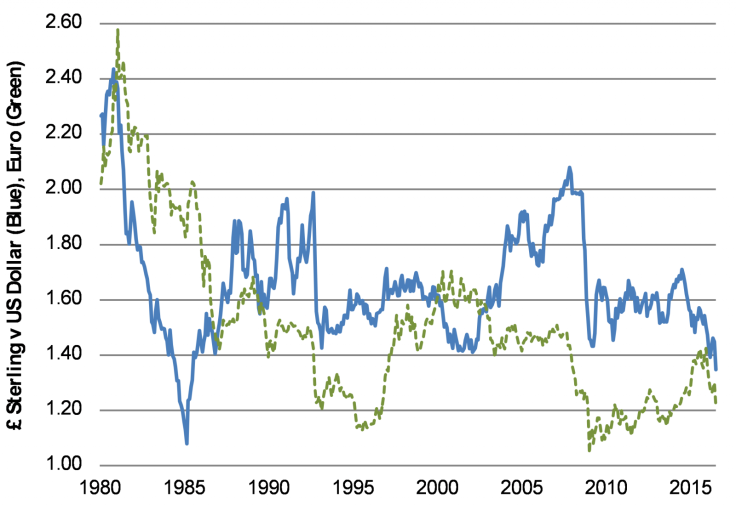

The pound sterling is probably the best example of this sharp readjustment by financial markets to this new reality, with the pound falling to a new 31-year low against the US dollar of $1.32 on Monday (Chart 1), and also suffering heavy losses against the euro too. If you haven't already bought your holiday money in preparation for this summer, then guess what – you are going to get a lot less for your pounds abroad now.

In the UK stock market, smaller companies have suffered more

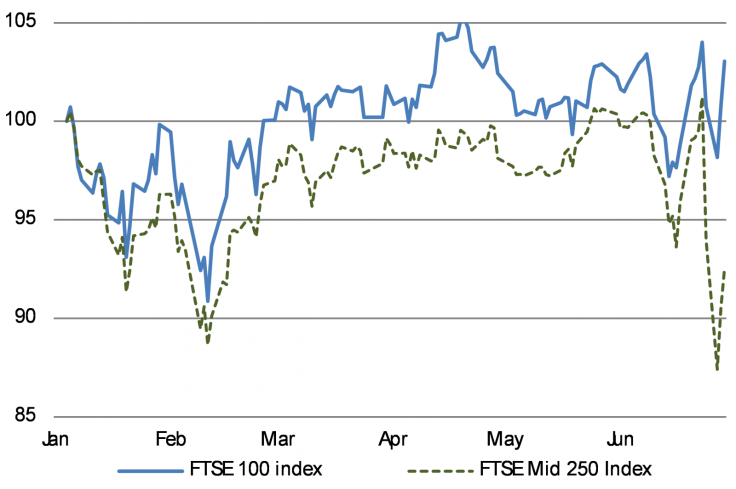

If we turn our attention to UK stocks and shares, we can observe that the flagship FTSE 100 index of the largest companies in the UK has actually not fared too badly.

If you look at Chart 2, you can see that in fact, the FTSE 100 index has gained over 3% since the beginning of this year, in spite of the EU Referendum result.

But why is this, when the pound has been hit so badly? Well, the main reason is the heavy global exposure of the largest companies that make up the FTSE 100.

Oil companies like Royal Dutch Shell and BP have the vast bulk of their operations overseas in oil- and gas-producing regions such as West Africa, the US and Canada and the Middle East, so are not really affected by the UK's domestic policies.

Similarly, HSBC is one of the largest banks globally, but has a huge footprint in Asia, the Middle East and the US, not to mention in Continental Europe (in France, for example). So again, while it has operations in the UK, this represents only a small part of the overall bank's revenues and profits.

In contrast, the FTSE Mid 250 index representing the 250 companies that are just below the largest 100 companies in size has borne the brunt of the post-Referendum pain in the UK stock market, with this mid-cap index 8% lower today than pre-Referendum Thursday (June 23) – the green dashed line in Chart 2.

Recession risk sectors hit hardest: Property-related, retailers, financial services

Industries with the greatest exposure to the domestic UK economy have suffered the most over the last few days.

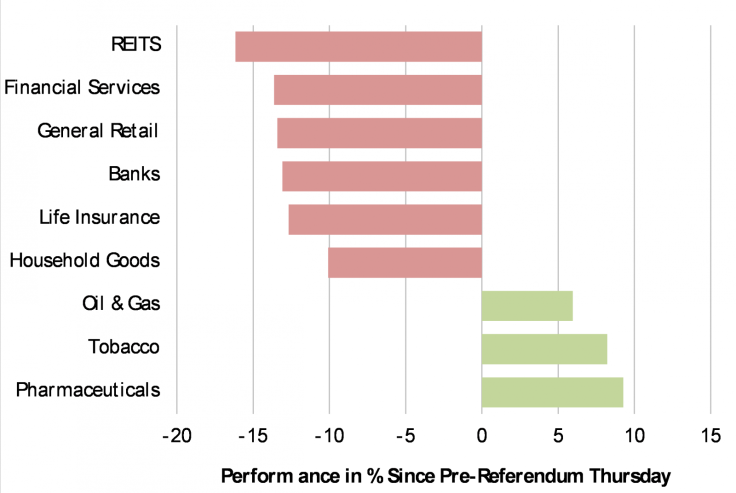

Chart 3 highlights that while global, defensive sectors like Oil & Gas, Pharmaceuticals and Tobacco companies have all actually enjoyed rising share prices since June 23, domestically-sensitive sectors like property companies, house builders and banks have lost more than 10% on average over these few days.

The reason for this is simple: the political and economic uncertainty that now hangs over the UK as a result of this vote hinders economic growth, as companies are now reassessing their investment and hiring plans in the UK, and may well be forced to relocate jobs and operations to other European Union countries.

Economists are forecasting a high likelihood that the UK will fall to zero economic growth or even recession by late this year, conditions where these domestic, cyclically-sensitive companies have under-performed in the past.

Four potential UK opportunities for the keen value investor

When turmoil like this hits financial markets, the sharp sell-off can create investment opportunities for value-oriented investors with a sharp eye for a bargain.

If the UK does not enter a deep recession, but instead sees a slowdown to zero growth at worst by winter this year, then the share prices of many domestic companies may prove to have overreacted currently.

I would look at the following UK companies and sectors:

- Hammerson (property; UK code HMSO) is interesting, as 27% of its commercial properties are actually in France, so it has a relatively high exposure to the Eurozone today. Hammerson offers a juicy 4.6% dividend yield for income, and is valued at a discount to net asset value of 29%. That means that you can buy £1 of Hammerson property assets for just 71p today.

- Hansteen (property; code HSTN) , although smaller than Hammerson, Hansteen is potentially even more interesting as it actually has 58% of its property exposure in Germany, and another 22% in the Netherlands, with only 17% exposure in the UK. And Hansteen offers a generous 5.5% dividend yield today.

- Halfords (retail; code HFD) is a retail stock that has lost 20% since June 23, with a share price that has fallen to just 322p today. The average analyst share price target is 390p (21% higher), the price/earnings ratio is very cheap at under 10 times earnings, and Halfords could get a boost from the Rio Summer Olympic Games if Team GB does well as expected in the cycling events.

- Schroders (asset management; code SDRC) is a very high quality asset management company with a very strong brand in investment funds, a strong track record in managing their business well and which has lost 15% in share price terms since June 23. They have raised or maintained their annual dividend payments every year without fail over at least the last 15 years (even through recession), and offer a 5.1% income yield from dividends today.

Investing at times like this is clearly for the brave; but it is also at times like this when the best investment opportunities can be found (when investor fear is widespread).

© Copyright IBTimes 2024. All rights reserved.