Kingfisher to Deliver Robust FY Earnings, on Track to Emerge as Industry Leader

Kingfisher, the home improvement retailer, is keen on to reposition its business as the industry leader and expects to deliver FY profits in line with analysts' expectations for the year ended January 28, 2012 on Thursday.

Looking ahead the group expects the global economic outlook to be uncertain and will continue to remain focused on self-help measures to trade the business effectively, whatever the market conditions. Its medium-term ambition remains to reposition the group's business as the industry leader at the forefront of innovation, helping its customers have "better homes, better lives."

The home improvement products and services group reported a 2.2 percent rise in Q4 sales, up 4.0% in constant currencies (Like-for-Like up 0.9%) and expects full year adjusted profits to rise around 20% in line with current analysts' estimates and it also announced its updated organisation structure in January, 2012.

Commenting on trading, CEO Ian Cheshire said: "With sales growth in each of our three main divisions and further solid profit growth in our final quarter we have ended another challenging year in robust shape. Our established programme of self-help initiatives has continued to serve us well and so we expect to announce full year adjusted profit in line with the current consensus of analyst expectations."

According to economic consultancy Independent Cost Benefit Analysis, it is expected that British retailers will be able to cash in on the influx of tourists visiting the Olympics this year, with the government set to relax Sunday trading laws during the games, in a move it hopes will deliver a £90 million boost to stores.

A rapid expansion in existing markets and the development of a common range of products to improve profit margins will be key themes for Kingfisher when it sets out the next phase of its strategy along with full-year results on Thursday.

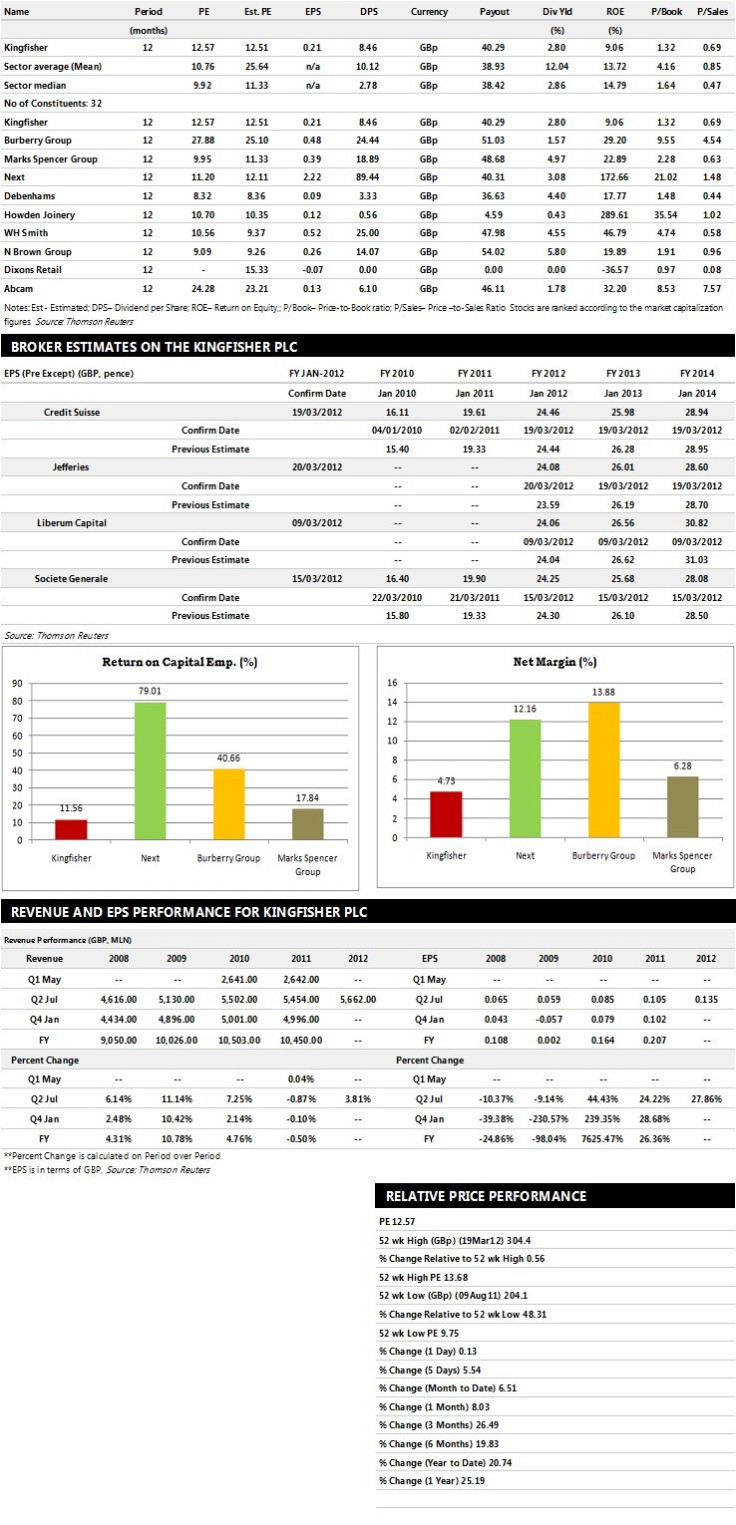

Below is a summary of sector comparisons in terms of price earnings, earnings per share, dividend per share, dividend yields, return on equity and price-to-book ratio. The table explains how the company is performing against its peers/competitors in the sector. The table below represents ten companies based on market capitalisation.

Brokers' Views:

- J P Morgan raises price target to 361 pence from 329 pence and assigns 'Overweight' rating

- Credit Suisse recommends 'Out Perform' rating on the stock with a target price of 310 pence

- Jefferies assigns 'Hold' rating with a target price of 310 pence per share

- Societe Generale gives 'Out Perform' rating with a target price of 310 pence per share

- Liberum Capital assigns 'Buy' rating with a target price of 345 pence per share.

Earnings Outlook:

- Jefferies estimates the company to report revenues of £10,826 million and £10,866 million for the FY 2012 and FY 2013 respectively with pre-tax profits (pre-except) of £800 million and £862 million. Earnings per share are projected at 24.08 pence for FY 2012 and 26.01 pence for FY 2013.

- Credit Suisse projects the company to record revenues of £10,582 million for the FY 2012 and £11,057 million for the FY 2013 respectively with pre-tax profits (pre-except) of £800 million and £850 million. Profit per share is estimated at 24.46 pence and 25.98 pence for the same periods.

- Societe Generale expects Kingfisher to earn revenues of £10,831 million for the FY 2012 and £11,052 million for the FY 2013 respectively with pre-tax profits of £805 million and £850 million. EPS is projected at 24.25 pence for FY 2012 and 25.68 pence for FY 2013.

© Copyright IBTimes 2024. All rights reserved.