Emerging Markets Turbulence May Signal 'Sudden Stop' Says Morgan Stanley

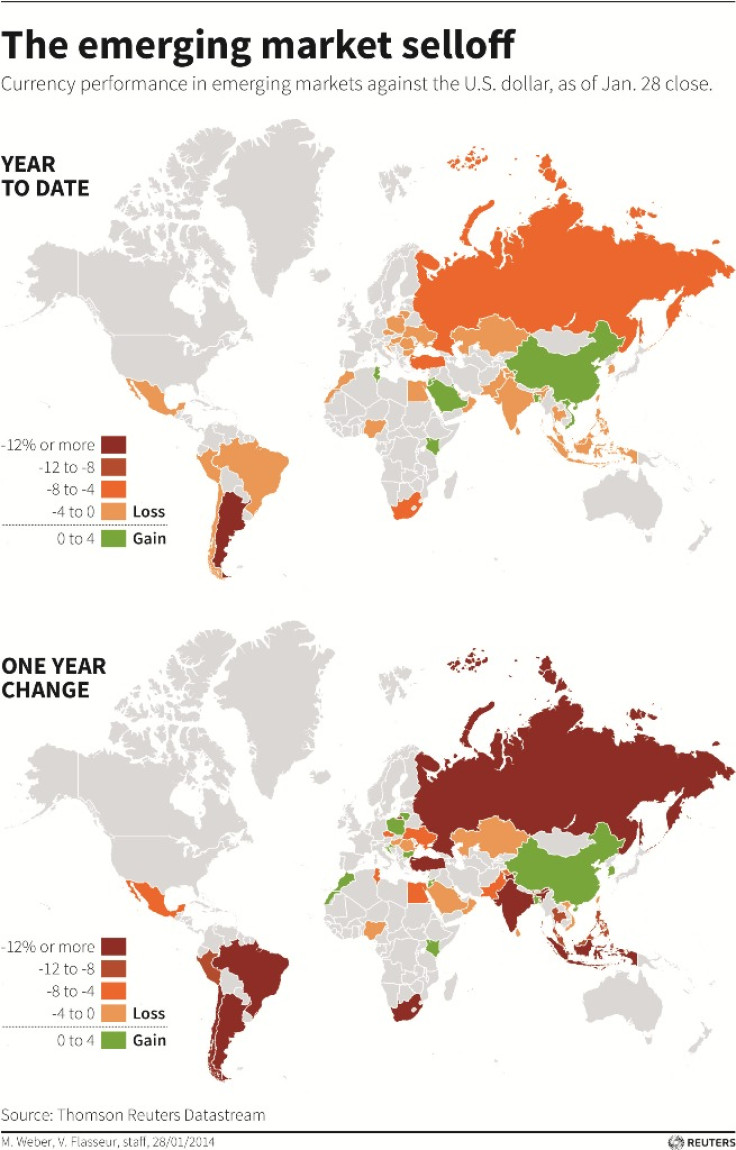

Brazil, South Africa, Turkey and Ukraine are the emerging markets most at risk of a "sudden stop", which refers to an abrupt halt of capital flows into a country, according to Morgan Stanley.

India, Indonesia, Mexico and Thailand could also face such a phenomenon as market players turn their backs on emerging markets, London-based economists Manoj Pradhan and Patryk Drozdzik said in two reports to clients earlier in the week.

Their comments came as central banks in India, Turkey and South Africa raised benchmark interest rates to defend their currencies.

A "sudden stop" is defined as a halt or even a reversal in capital flows into a country, cutting access to international financial markets for a prolonged period and weakening the economy. The term is often linked to the 1995 work by late MIT professor Rudi Dornbusch.

The Morgan Stanley economists assessed risk by studying factors such as the dependence on capital inflows and credit, the size of a country's current account deficit, freedom for policy and exposure to China.

The countries most in danger have to determine how they would fund their budget and trade gaps and whether they can turn to new sources of expansion, the economists said.

The authors also advised market participants to track political developments and the processes of reducing debt. Thailand, Turkey and Ukraine have all suffered political unrest.

Societe Generale Cross Asset Research said in a note to clients: "Since cumulative inflows into EM equity funds reached a peak of $220bn in February last year, $60bn of funds have fled elsewhere. Given the exceptionally strong link between EM equity performance and flows, we think it plausible that funds are currently withdrawing double that from EM equity."

"EM bond funds face a similar fate. We see no early end to EM asset de-rating. Furthermore, the [US Federal Reserve] remains assertive on execution of tapering despite recent turmoil within the EM world, which spells more turbulence ahead."

EM Currencies

Commerzbank Corporates & Markets said in a note to clients: "In spite of the current problems, we still do not envisage an EM-wide currency crisis. There are risks, though, in those cases where the markets are not convinced that a central bank is pursuing a sufficiently restrictive monetary strategy that will lead to a sufficiently rapid and sustainable reduction in the current account deficit."

"BRL is proving relatively robust in this respect. An early change of the monetary stance to a restrictive course has taken effect, and there is a good chance of the recent BRL depreciation being short-lived, though it will not of course be able to shake off entirely the contagion effect from general EM currency weakness."

"The outlook for TRY and ZAR is different, though. Sudden rate hikes aimed at alleviating depreciation pressure do not engender confidence. If the market does not trust a central bank to combat large current account deficits on a sustainable basis and raise returns on imported capital on a permanent basis, the authority in question will not succeed in maintaining a stable currency. Both the CBT and the SARB will have to proceed with efforts to regain the trust of the markets in a climate of a changing Fed policy," the German bank added.

UniCredit Research said in a note to clients: "But even assuming EM economies continue to take their medicine, 2014 will remain a volatile year. The election cycle is busy, with elections scheduled in Turkey, Brazil, India and Hungary, amongst others. More importantly, many EMs have exhausted any 'easy' sources of domestic growth as they sought to compensate for a weaker external environment in recent years.

"For example Turkey's credit growth over recent years was fuelled initially by an increase in the loan to deposit ratio above one and followed by a sharp increase in external borrowing abroad. This is unlikely to be repeated again. China has pushed private credit (including local governments) significantly higher, in part via opaque financing vehicles."

"Rolling some of this financing is proving problematic. Hungary has largely exhausted its scope to provide the economy with a positive impulse via interest rate cuts while commodity producers such as South Africa and Russia must adjust to a world of stable to negative terms of trade, rather than improving terms of trade," according to UniCredit.

"There is light at the end of the tunnel. If policy makers prove willing to adjust to a period of lower growth, differentiation will increasingly become a theme once again. Central Europe provides a positive example of this in recent quarters. But at this stage, there is still more work to be done," the Italian firm added.

In their 29 January report, after the rate increases Turkey and South Africa, Pradhan and Drozdzik wrote: "this new policy awareness is by itself a positive and a step in the right direction."

In their 27 January report, the economists said: "While the risk of a sudden stop is higher in some economies and lower in others, EM economies remain exposed to the risk. If policy makers don't enforce the change and reforms that are needed to generate a new model of growth, asset prices will adjust by as much as is necessary to generate that change."

Risks to Eurozone

The Eurozone faces a huge risk from the recent outburst of emerging-market anxiety.

The region in 2013 exported the equivalent of 3.1% of GDP to Brazil, Russia, India, South Africa, Indonesia, and Turkey, Julian Callow, chief international economist at Barclays, told Bloomberg. That compares with 2.4% for Japan and 1.3% for the US.

By contrast, the Eurozone's exposure to the thus far non-stressed emerging market economies was 4.7%. America's was 3.3% and Japan's 6.6%.

© Copyright IBTimes 2024. All rights reserved.

-

Doug McMillon Unloaded Walmart Trucks For $6.50/Hour In 1984, Now He's The CEO

-

Utah Couple Doesn't Know Cat Jumped Into Amazon Package, Accidentally Ships It to California

-

How Are Female Tech Firms Fighting the Employment Crisis in the West Bank?

-

Italian PM Has British Newborn With Heart Defects Airlifted to Rome for Treatment Unavailable in UK