3 reasons why BHS, Austin Reed and other UK retailers are struggling

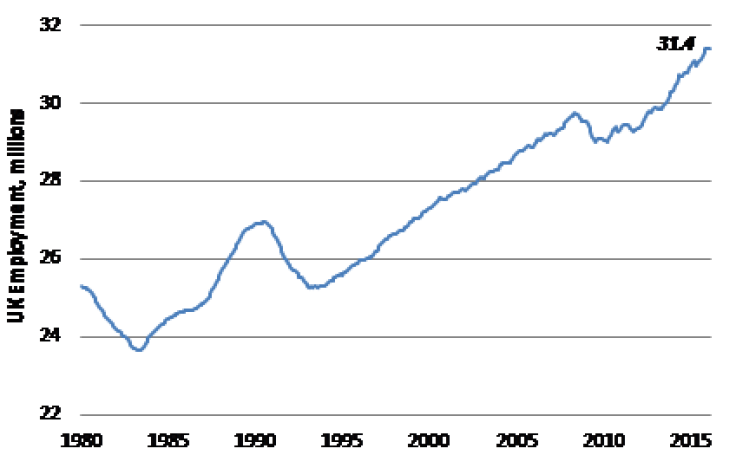

With UK employment officially at record highs (Chart 1), the domestic UK economy should be doing well.

But something is not quite right: the Retail sector is clearly suffering, judging by the potential insolvency of High Street department store chain BHS and menswear retailer Austin Reed. So why is our relative prosperity not translating into better sales and profits for UK retailers?

Not just a BHS and Austin Reed problem: other retailers suffer too

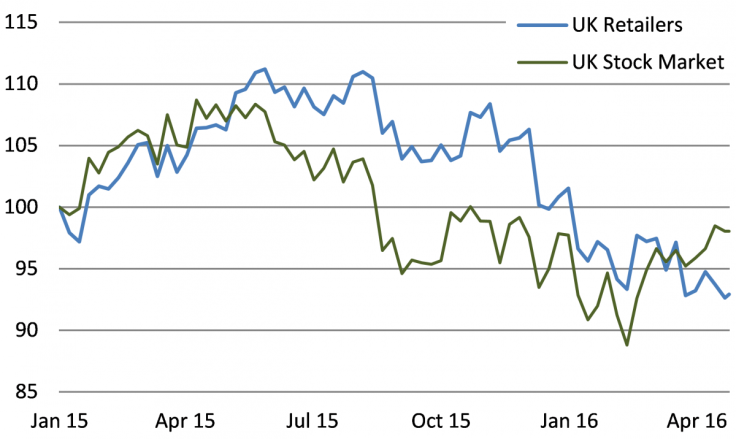

Since May of last year, retailing shares have suffered alongside the benchmark FTSE 100 index (Chart 2).

However, unlike the broader stock market, UK retailers have not enjoyed a recovery over the last couple of months. Instead, the General Retailers sector (including the likes of Marks & Spencer and Next) has continued to fall, hitting a new low last week.

There are a number of factors behind this under-performance:

- Slow wage growth. Despite a record-high level of employment in the UK economy, wages are not growing fast at all. Normally, with unemployment this low, you would expect wages and salaries to rise faster as employers struggle to fill positions. But this is evidently not happening at the moment, thus households are not seeing a big rise in spending power.

2. UK retailers lag the stock market Bloomberg Introduction of the Living Wage. The one area where wages are set to rise is at the minimum wage level. The introduction of the living wage (£7.20 per hour for workers aged 25+), 50p per hour above the prior National Minimum Wage, will boost low incomes. But retailers, who employ a lot of people at relatively low wage levels, will have to pay this higher living wage, hurting profits.

- Continued pressure from the internet. There is a continued shift in shopping habits away from "bricks and mortar" stores on the High Street towards web-based shopping sites such as Asos and boohoo.com, based on an attractive combination of convenience and low price. This continues to eat away at the profitability of traditional store chains, even as they invest in their own online web sites.

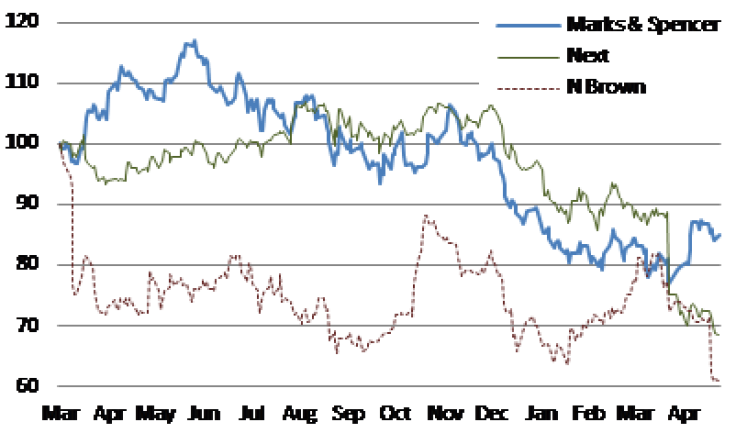

The result of these three pressures on profits is weakness in the share prices of such High Street stalwarts as Marks & Spencer, Next and catalogue retailer N Brown (Chart 3).

But Halfords and Kingfisher stand out

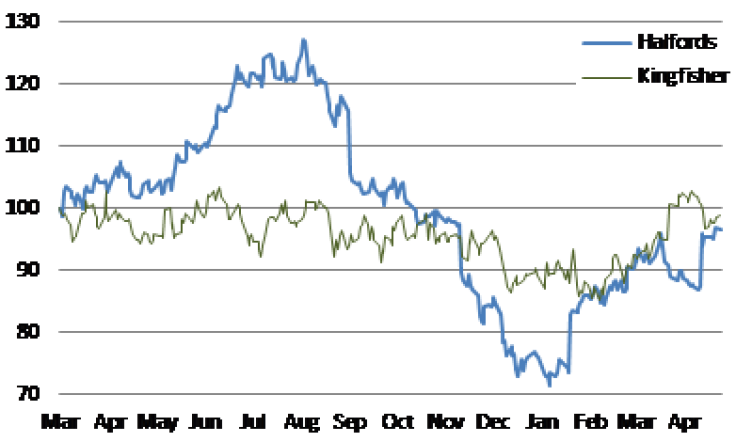

Resisting these profit pressures are a couple of specialist retailers, Halfords (UK code: HFD) and Kingfisher (UK code: KGF).

Halfords has a couple of very strong niches in which it operates: car parts and accessories, and bicycles. It is the UK's number 1 retailer by some distance in both categories, and this niche positioning allows Halfords to earn strong profit margins. Steady growth is also coming from its autocentres, where it repairs cars and bicycles.

As a result of the like-for-like sales growth that Halfords has managed to achieve, Halford's share price has rebounded some 25% from its mid-January low (Chart 4).

Kingfisher, the owner of the B&Q DIY store chain in the UK and its French DIY equivalents Castorama and Brico Depot in France, has also performed better than most UK retailers on the back of rising UK house prices, which have spurred homeowners to spend on renovation and upgrading of kitchens and bathrooms.

According to Retail Week, for the week ending April 17 homeware sales have done well, led by homeware accessories and decoration. This current trend should prove good news for B&Q, and should remain in place so long as UK house prices drift higher.

Bottom line: the UK retail sector is a place where investors currently need to take particular care. Halfords (HFD) and Kingfisher (KGF) remain two of the few retail stocks which continue to perform well in spite of the tough general retail environment.

© Copyright IBTimes 2024. All rights reserved.

-

US Couple Donates $121M To Help Fund College Scholarships at a Ohio University, but There's a Catch

-

Fitness Instructor Sentenced To 11 Years In Prison For Demanding An End To Saudi Arabia's Guardian Laws

-

Thai Official Suspended After Husband Catches Her In Bed With Adopted Monk Son

-

Jakarta Is Sinking: Indonesia's $30B Plan To Relocate 11M Residents To New Capital Starting October 2024