Exaggerated Pre-Crisis Financial Sector Performance Causing UK Economy's Productivity Decline

Britain will not return to the levels of growth seen in the build-up to the 2008 financial crisis because the level of productivity being reported was misleading and unsustainable, according to a new report by a leading economic think tank.

Overstated productivity, particularly in the financial sector, helped give a false impression of the strength of the UK's GDP and so some of the post-2008 decline can be put down to this excess being cut away permanently, said the Centre for Economics and Business Research (CEBR).

Collapsing output in sectors where productivity is demand-driven has also weighed down the economy. Demand has been seriously hampered by a lack of confidence among businesses and consumers who are conscious of the weak and uncertain global economy.

"Both are reasons we should be less worried about today's level of productivity than we might otherwise have been," said Douglas McWilliams, CEBR chief executive.

The UK is in its longest double-dip recession since the Second World War. It is the second recession in four years as the country struggles to return to consistent growth.

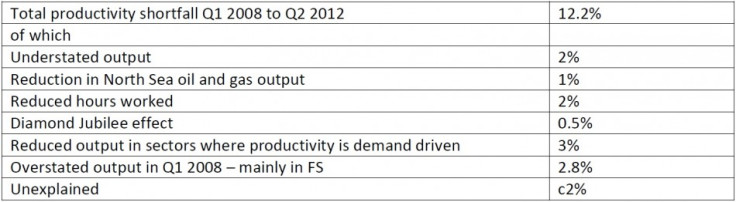

Of a total productivity shortfall of 12.2 percent from the first quarter to 2008 to the second quarter of 2012, 2.8 percent is accounted for by overstated productivity in the three months to March 2008.

A further 3 percent is because of demand-reliant output falling.

The bloated productivity figures in Q1 2008 are mostly because of the financial sector, which had a catastrophic breakdown and led to many banks requiring taxpayer-funded bailouts to keep it propped up, said CEBR.

CEBR analysed productivity data from the City, as well as bonus, employment and merges & acquisitions figures from the financial sector.

They calculated the loss of productivity from 2008 to 2012 to be 3.1 percent.

This means the figure for productivity in the City during the 2007/2008 year is overstated by 2.8 percent.

"Some of this was un-renewable business; some profits being accounted for that subsequently had to be written off; some euphoric overcharging," McWilliams said.

Other reasons the UK has seen its output decline overall in recent years is lower oil and gas output, the bank holiday effect from the additional day off for the Queen's Diamond Jubilee, and a reduction in hours worked as full-timers get less overtime and the number of part-time workers goes up.

"Looking forward, the figures are bad news in one sense," McWilliams said.

"They imply that one should be rather more pessimistic about future productivity growth in a new world where GDP growth could easily be sluggish and that there is only a relatively small productivity bounce-back in prospect as underutilised labour is put to better use.

"But at the same time this is probably less bad news for the future of employment and unemployment in the UK. Employment will be higher, given sluggish GDP growth, than might have been expected. And as a result unemployment will not rise as quickly.

"On balance therefore, the challenge to raise living standards for the UK remains the same as ever - the labour force needs to improve its skills, investment is required to raise capital intensity and improved organisation remains necessary to obtain higher total factor productivity.

"We should not rely on some sort of automatic bounce back to the pre-2008 circumstances to make us better off."

© Copyright IBTimes 2025. All rights reserved.

- MOST READ