Global Bond Funds See Biggest Outflows In Two Decades

Global bond funds saw the biggest outflows in two decades in the first three quarters of this year as hefty interest rate increases by central banks to tame inflation sparked fears of a recession.

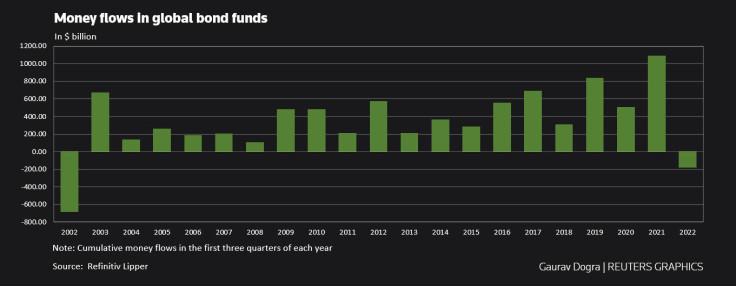

According to Refinitiv Lipper, global bond funds faced a cumulative outflow of $175.5 billion in the first nine months of this year, the first net sales in that period since 2002.

Money flows in global bond funds

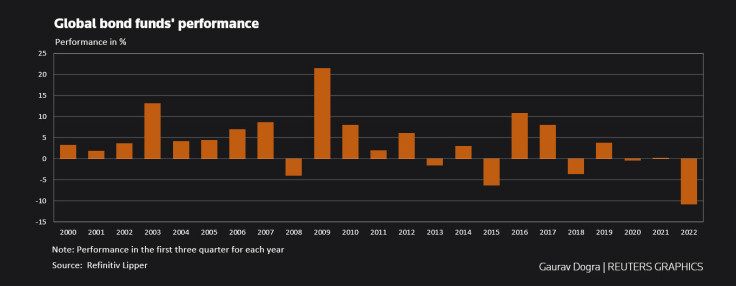

Global bond funds declined by 10.2% on average in their net asset values, their worst slump since at least 1990, the data showed.

Global bond funds' performance

Governments and companies have borrowed heavily in the past few years, taking advantage of ultra-low interest rates, and they now stare at bigger interest liabilities due to a rise in yields.

"The combination of high debt levels and a rise in interest rates has reduced investors' confidence in the government's ability to pay back debt, which has resulted in the massive outflows we are seeing," said Jacob Sansbury, CEO at Pluto Investing.

He added that outflows from bond funds might continue into 2023, as a reduction in interest rates and reduced debt loads are unlikely.

Emerging market bonds faced an outflow of about $80 billion in the first three quarters of this year, while U.S. high yield bonds and inflation-linked bonds witnessed net sales of $65.81 billion and $16.44 billion, respectively.

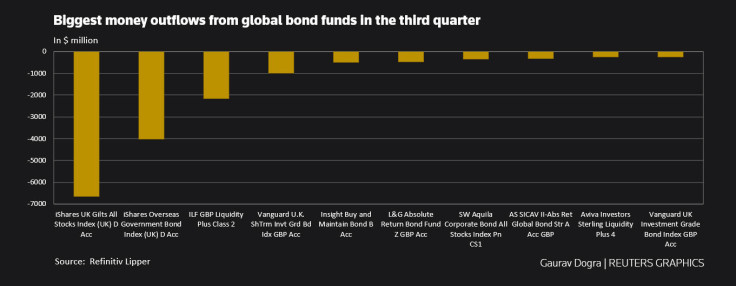

The iShares UK Gilts All Stocks Index (UK) D Acc recorded outflows of $6.67 billion in the last quarter, while the ILF GBP Liquidity Plus Class 2 and Vanguard U.K. Short Term Investment Grade Bond Index GBP Acc fund saw withdrawals of $2.16 billion and $993 million respectively.

Biggest money outflow from global bond funds in the third

quarter

BONDS ATTRACTIVE NOW

However, some funds managers said bonds looked attractive after the slump this year.

The ICE BoFA U.S. Treasury Index has fallen 13.5% so far this year, while the Bloomberg Global Aggregate Bond Index has shed about 20%.

"The yield cushion now protects the investor against negative total returns significantly more than it did at the beginning of the year," said Jake Remley, portfolio manager at Income Research + Management.

"This almost certainly makes the prospects for bonds better between now and year-end, even if interest rates continue to rise as briskly as they have over the past 9 months."

The yields on 2-year and 10-year U.S. Treasury bonds stood around 4.12% and 3.68% respectively on Wednesday, compared with 0.7% and 1.5% at the start of the year.

Similarly, the yield on the ICE BofA U.S. High Yield index, the commonly used benchmark for the junk bond market, stood at 9%, compared with 4.3% at the start of the year.

"Some bonds have become the proverbial 'babies thrown out with the bathwater' and offer compelling value at these levels," said Ryan O'Malley, portfolio manager at Sage Advisory Services.

"However, it's important to note that there will likely be further credit stress in many corners of the bond market and risk management is paramount in these uncertain times."

Copyright Thomson Reuters. All rights reserved.

- MOST POPULAR IN Markets