BoE Inflation Hearings: Will Carney Drive Sterling Towards $2?

The Bank of England governor, Mark Carney, and some of his fellow MPC members will address the Treasury Committee on 24 June where the rate setters will be grilled on their stance on inflation and related matters.

The market will be looking for more cues for Sterling as the governor has already given a big verbal boost to the currency, which triggered a fitting move in it.

In this year's Mansion House speech, delivered on 12 June, Carney said bluntly that the central bank is likely to hike the bank rate sooner than the market has been anticipating.

But the next signal markets received from the central bank had a neutralising effect. The BoE minutes released on 18 June spoke about headwinds in the growth path and ascertained the need to keep rates low for some more time.

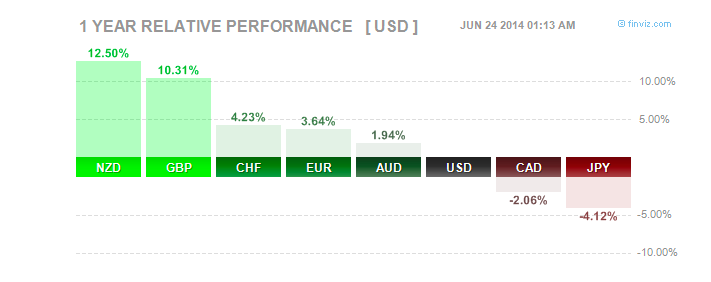

The Currency Rally

Sterling had an immediate 100-pips jump from near 1.6840 against the US dollar after the Mansion House speech and then continued upward to hit the 1.70 mark.

The move got stalled by the MPC minutes and GBP/USD dropped to a low of 1.6920.

But then came the Federal Reserve policy decision, disappointing the market which had been anticipating more hawkish signals from the world's most influential central bank.

A view of easier dollar liquidity for a longer term, bolstered by the FOMC on 18 June, helped risk sentiment globally and strengthened the British pound to as high as 1.7064 against the greenback, a five-year high, by the next day.

GBP/USD has rallied 1.38% to its 19 June peak since the Mansion House speech. Data by Finviz.com shows that pound has strengthened more than 10.3% so far this year against the greenback, second only to NZD in G10.

What Numbers Say

Data released in June showed strong growth indicators but slowing price pressures in UK.

Industrial output grew 3.0% year-over-year in April, faster than 2.5% in March and exceeding analysts' forecast of 2.8%, data on 10 June showed. The three months to April ILO unemployment rate came in at 6.6%, lower than the consensus of 6.7% and previous month's 6.8%, as per the data released the next day.

However, core consumer price index slowed to 1.6% on year from 2.0% in April when analysts were expecting a rate of 1.7%, data on 17 June showed.

The industrial trends survey by the Confederation of British Industry (CBI) released on 19 June provided an index of 11 compared to the market consensus of 3 and previous month's 0.

Retail sales growth had also slowed more than expected in May, data on 19 June showed, but analysts said the overall trend in sales has been strong over the past few months.

The impact of negative numbers on the pound has not been significant of late, as the market focused on the rate guidance by Carney, better growth scenario in the UK as well as the broad dollar weakness and its effect on global risk appetite.

Technical Outlook for Sterling

Above 1.7064, GBP/USD will target 1.7350, the 50% retracement of the November 2007 to January 2009 downtrend, ahead of the 61.8% level of 1.8265.

A breach of this will open 1.8700, 1.9000 and 1.9480 ahead of the 2.0 mark, last touched in November 2007.

On the downside, the pair has first major support at 1.6384, the 38.2% retracement, ahead of 1.5854 and 1.5233, the 23.6% level. A break of that will confirm a downtrend and the next targets will be 1.4813 and 1.4230 ahead of 1.3503, the January 2009 low.

© Copyright IBTimes 2025. All rights reserved.

- MOST READ