How to realise the potential of blockchain in developing economies

Joel John, lead researcher for Blockchain-focused VC firm Outlier Ventures, looks at the history of blockchain's promise of financial inclusion.

The narrative is standard: poor woman in a remote part of the world receives a micro-loan from a foreign investor through a digital medium. She buys a goat, sells milk and begins earning money. Reinvests the money into additional sources of income and before you know it, she's climbing up the social ladder. All this, while providing her foreign investor with a better return on investment than anywhere else. Commonly referred to as "goat economics", this story has been retold in almost all financial inclusion literature. With the advent of blockchains, the narrative has added a trustless, distributed ledger. The recipe for tackling poverty is simple according to proponents in this corner of the globe:

- Take a distributed ledger with trustless, decentralised token mechanisms

- Hope the world's poor will move towards using the new ledger due to lower costs, cheaper credit and better security

- Create a marketplace for capital investments (eg: loans, remittances) to flow from richer regions of the world to third world economies. Call it capital osmosis.

- Ignore regulations and have a roadmap that includes loans, insurance, payments, savings & bank accounts

- Use huge market sizes (eg: 5 Billion "unbanked") without segmenting target market or understanding market requirements.

This might sound reductive, but this has been the pitch for many "financial inclusion" oriented start-ups leveraging blockchains since early 2012. That is not to say that each startup does not have the best intentions because ultimately no entrepreneur targeting financial inclusion is doing it because it will be easy. They are doing it because they want to change the world and help integrate every person on earth into the financial system to improve their lives. This is a noble and honourable goal. We hope that by providing some historical context and a few key learnings, startups can better meet the needs of the excluded and we can all achieve the goal of financial inclusion faster.

3 Generations of Start-ups. Same Theme.

1. Generation 2013

One of the earliest learnings in blockchain backed financial inclusion came from Btcjam. The start-up had made its entry to market as early as 2013 and was backed by the likes of Ribbit, Pantera and 500 start-ups. The promise was simple:

- Create a marketplace for lenders and those seeking credit.

- Use a reputation management system and repayment rates to track credit worthiness.

Although the idea worked on paper, the start-up had to shut shop due to low repayment rates and a substantial number of investors losing money. There was even a marketplace for individuals seeking to "sell verified, credit worthy" accounts to conduct fraud. The issues here were: centralized reputation and identity management combined with a lack of collateral and means to recover money lead to a high rate of fraud within the ecosystem.

2. Generation 2014–2016

The next batch of start-ups (born between 2014–2016) oriented towards financial inclusion through cheaper payments and remittance. Notable survivors from this era are Rebit and Bitpesa. The value proposition was to combine bitcoin's low cost of remittance with minimum requirements for banking infrastructure. This in turn allows individuals to send and receive money at a fraction of the cost charged by traditional enterprises. Bitpesa pioneered the model with the help of telephone based remittances. While metrics are limited, crunching numbers from Bitpesa's landing page reveal the challenge of getting traction. The site states the platform has over 6000 users, spread across 85 countries and a total of 17,000+ transactions. This accounts for very roughly ~3 transactions per individual through the platform. This is likely not enough to support a growing business, and it makes sense that BitPesa as well as others have evolved their offerings to include exchanges. From a functional perspective, this increases liquidity and drives new revenues, but more importantly it aggregates the payment and exchange layer of the value chain. As Marc Andreessen says: "only two ways to make money in business: One is to bundle; the other is unbundle."

3. Generation ICO

The current generation of start-ups (What we are now calling the post ICO era) working towards financial inclusion take things one step further. Instead of relying on bitcoin, they use ethereum to issue tokens that are then (usually) used for payments settlements. Instead of centralising reputation management, they store it on a distributed ledger which cannot be erased. Most importantly, they combine network effects and incentives in a new fashion. Pioneers in the space are WeTrust & Humaniq. WeTrust allows individuals to create lending circles with the help of smart contracts. This allows communities to pool money and settle loans internally atop a trustless ledger. Humaniq on the other hand aims to "issue" coins for early adopters of the platform and create financial infrastructure with the help of biometric scanners and mobile devices. It is too early to call either of them a success as they have alot of work to do to achieve their stated goals. The case with many of these startups is not their will or motivations, but rather the practicalities on the ground make financial inclusion very difficult.

The Fix: Trust, Incentives & On-boarding

On a parting note made by BtcJam dated 25 May, 2017, the start-up left the key reasons behind it's closure: " The regulatory challenges around Bitcoin and the difficulties we faced in introducing Bitcoin technology to poor communities around the world are simply beyond our capacity."

In spite of issuing loans worth 60,400 Bitcoins ($430 million in present value) through 20,600 loans in 122 nations, the firm shut due to the difficulties they faced in on-boarding the world's poor on a blockchain. The main challenges were: trust, incentives, and on-boarding.

1. Trust

A year back the government of India "decommissioned" 86% of the nation's fiat currency. Individuals that were in remote regions with only fiat holdings for savings (due to lack of banks) were left estranged for months until the new notes became commonly available. Over 100 people died across the nation between waiting in lines for the new notes and being unable to pay for medical bills (Let that sink in for just a moment). This was the case with state backed currency in one of the world's fastest growing super powers. Observations from the capital markets of growing economies shows that individuals tend to invest in physical assets such as gold or real estate over currency or equity markets due to the lack of faith in a third party handling their money. In this scenario, saying "blockchains" and "digital money" can save their lives doesn't resonate the way some people think. Banking relationships in emerging economies are often built over generations. Monetary flow from physical currency to the digital realm would require individuals putting their complete faith in technology they can't understand and individuals they cannot see. The "unbanked" often do not have income they can experiment with. The cost of losing money could often be chronic hunger. In such a scenario, the promise of a token economy amongst the world's poor remains weak.

2. Incentives

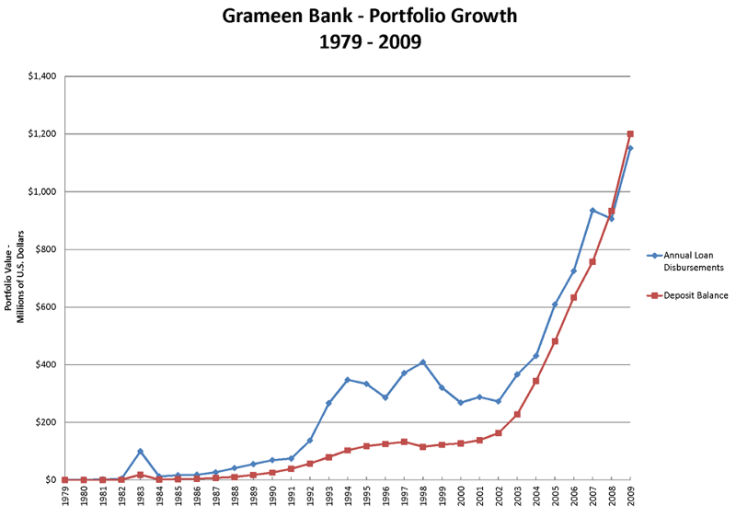

Changing the world's poor from using physical currency to blockchain based tokens would require incentivising them sufficiently to make the change. Any practice that requires a change of habit would have to be forcefully enforced or have an obvious advantage visibly present. While cheaper remittance, better security and immutable records have their advantages, none of these might motivate individuals to switch just yet. As an example for this, consider Muhumud Yunus' experience setting up Grameen Bank. Through his memoir titled "Banker To The Poor" the Nobel Prize winner explains how the poor did not believe someone would offer cheap loans to begin with. It took him constant nudging, active presence locally & close to 12 years before the project saw major traction.

In order to on-board individuals to the token economy, communities would have to be activated locally with incentives. One cannot build financial infrastructure in a remote corner of the globe and anticipate individuals sitting half way across the world to embrace it. Studying how Multi-level marketing (MLM ) and ponzi schemes have picked up steam in these nations would be a good indicator of what would tick when it comes to consumer adoption. Indian scams like Gainbitcoin have attracted over a billion dollars over the past few years through a network of advocates and local presence. All this, while having flawed economics, zero sound investments and no actual product to sell. If blockchains are to be adopted amongst the world's poor, the incentives (or delta of the experiences prior to blockchain) need to be visibly larger. The average start-up working on financial inclusion tends to forget that solutions for the poor cannot be developed from some far-flung tech hotspot. The deployment should be organic, local & consist of proactive partnerships between government bodies, enterprises and local communities.

3. On-boarding

India is believed to have more sim cards than individuals with access to toilets. This sums up the state of things in growing economies. These are regions with increasing connectivity, but a lack of fundamentals such as literacy, sanitation and crucial infrastructure for identity. In such a scenario, claiming the rise of connectivity would lead to an adoption of blockchains in poorer segments could not be farther from the truth. To begin with, emerging products focused on the market segment need to be in the native language of the end user. Enterprises providing "Language as a Service" would be crucial in converting products to be more vernacular. In addition to this, a network of local product ambassadors would be required. Taking cues from Grameen bank again, the micro-finance behemoth was able to set itself up for success owing to the network of young, energetic individuals it employed during its early stages. Blockchain oriented enterprises focusing on the world's poor could possibly generate employment in these regions hiring individuals that are paid on basis of traction generated. They could help with everything ranging from AML/KYC to technical issues with a distributed app. India's Life Insurance Corporation became one of the nation's largest money managers by raising a battalion of "agents" that were incentivised on basis of performance

What Next?

The rise of blockchains could create measurable impact amongst the world's poor. However, it is not to be seen as the holy grail that fixes all problems. Systemic issues owing from culture, geography and community barriers will hinder the rate of adoption. Porting the world's poor towards immutable ledgers will not be solely about culture but a disruption of the systems and processes conventional finance has set in place over decades if not hundreds of years. What we have now is the foundational layer for this change to occur in poorer sections of the society. And that's pretty much it. Be it the Gates Foundation collaboration with Ripple or the all new "IndiaChain" that is aiming to solve everything from identity to agriculture. All blockchain based (and arguably all technology) solutions have their limits when it comes to these markets. As an example, consider Facebook's attempt at providing "free internet" in India. Through disregarding net-neutrality and engaging with policy makers whilst ignoring user sentiments, the social media behemoth ended up with nothing to show in spite of collaborating with some of the largest companies in the nation. Entrepreneurs and capital hoping to make a dent in these markets should respect the limits of software and work in sync with policy makers and local communities to make the change possible.

Blockchains can well be the wheels on this vehicle of change, but as with every instance of social transformation in the past—the engine will still have to be local leaders and communities that stand up and make it happen.

Notes

1. The article takes India as a backdrop for examples of the barriers in growing economies. Different regions will have unique issues owing to varying cultural, geo-political and socio-economic situations.

2. Start-ups mentioned in the article were pioneers in their own respect for choosing to pave new ways in emerging markets long before blockchains "were" cool. We hope it is only a matter of time before some of them find the ideal product market-fit and scale successfully.

- MOST READ