UK Landlords Yields Soaring as Buy to Let Loans Flood Market

Landlords across Britain are seeing bumper yields on their properties amid the market being flooded with Buy to Let loan products.

According to Mortgages for Business' Complex Buy to Let Index, gross yields on buy to let properties which only have a single tenancy agreement, stands at 5.9% as of third quarter 2014. However this is a slight fall from 6.3% in the second quarter this year.

However, larger multi-unit blocks (MUFBs), such as student houses which have locks on bedroom doors and as well as multiple tenancy agreements, saw yields reach 8.6% in the third quarter this year, up from 7.3% in the previous period.

"Rents on the plainest buy to let properties have not kept pace with rapid price rises in many areas, suppressing average yields," said David Whittaker, managing director of Mortgages for Business.

"This illustrates two key points for landlords – location matters – and the simplest investments are not always the most lucrative.

"Landlords with multiple tenants at each property can earn a better yield by providing what people need – often just a room rather than a whole flat. This must be done responsibly, for example HMOs often require a licence from the appropriate Local Authority, while landlords will also need a specialist mortgage product for more complex property types.

"However, if those hurdles are met, landlords can earn not just a higher, but often a more reliable return as part of a diversified investment."

Mortgage for Business also revealed that the number of buy to let mortgage products available is now at a fresh all-time record.

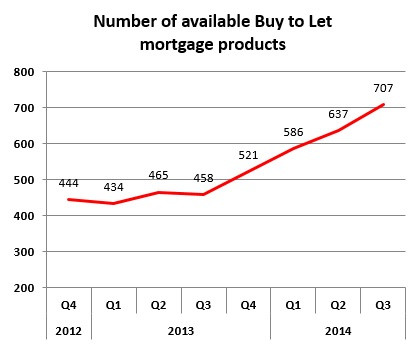

At the end of Q3, the number of available buy to let mortgages on the market stands at 707 separate loan products [Figure 1].

This is a hike from the previous record high of 637 in the second quarter of 2014.

One year ago, there were only 458 available mortgage products at the end of the third quarter 2013.

"A burst of competition in the buy to let mortgage market is facilitating a greater choice between different mortgages than ever before. We're seeing prudent landlords use that trend to find a fixed rate deal while rates are low.

"Landlords are aware of the approaching likelihood of not just one, but a series, of gradual Bank of England interest rate rises. While competition between lenders is keeping product rates low, now is the time to take advantage of that with a deal that cements the advantage of lower borrowing costs."

© Copyright IBTimes 2025. All rights reserved.

- MOST READ