Iran's Real Drops to New Low Amid Extended Nuclear Talks

Iran will continue to negotiate with the six world powers for a nuclear deal acceptable to both sides as the country struggles to sell its oil overseas in order to shore up economic growth and recover from a deepening currency crisis.

Iran's real is now trading 53% weaker from a year ago when the expanded sanctions took effect.

Iran, the United States, Britain, France, Germany, Russia and China have decided to extend the July 20 deadline by another four months to complete a long-term agreement.

The agreement is expected to find a solution to the disputes regarding Iran's nuclear plans and help it freely trade oil internationally.

"We have decided – along with the EU, our P5+1 partners, and Iran – to extend the Joint Plan of Action until November 24, exactly one year since we finalised the first step agreement in Geneva," US Secretary of State John Kerry said in his report on the negotiations held in Vienna.

"This will give us a short amount of additional time to continue working to conclude a comprehensive agreement, which we believe is warranted by the progress we've made and the path forward we can envision."

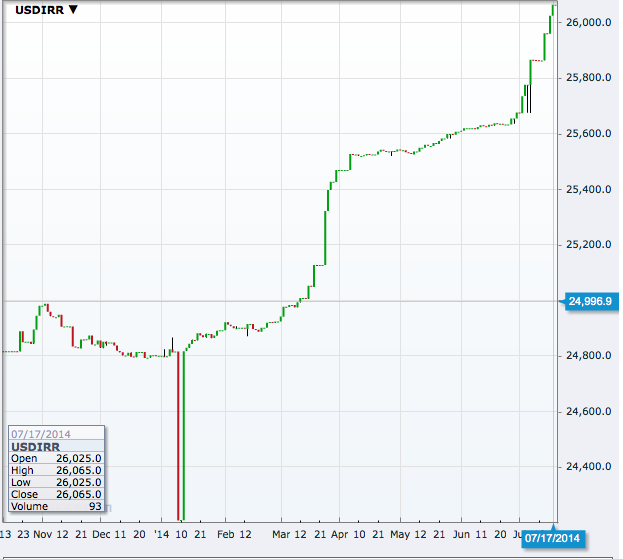

Iran's real, considered as one of the weakest currencies, has lost more than 1.6% against the US dollar so far in July and 4.85% until now this year. The USD/IRR pair traded at a record high of 26,065 on 18 July. [See the chart below.]

The global powers' decision to expand economic sanctions against Iran in July 2013 saw the real plunge by 50% to 24,800 from near 12,300.

Iran also has an active black market in its currency even as the central bank keeps its control over the interbank market. The gap between the official and black market rates has widened since the international sanctions came into force.

The Central Bank of Iran (CBI) identifies the Iranian year ending March 2013 as a precarious one, and listed a few factors that made it so, in its annual review published on its website.

"The impacts of highly expansionary economic policies of the years before, the effects of the Subsidy Reform Plan, sharp rise in exchange rate, and the international restrictions on Iran financial and trade transactions were only a few to mention," the central bank said.

"These developments led to a highly stagnant and inflationary environment in the domestic economy, although parts of these impacts were unveiled after the implementation of Subsidy Reform Plan."

Fall in GDP

Iran's GDP growth followed a sharp declining trend from 5.8% in 2010/11 to 3.0% in 2011/12 and then reversed to -5.8% in 2012/13, according to the CBI report.

Meanwhile, inflation rose sharply from 12.4% in 2010/11 to 21.5% in 2011/12 and 30.5% in 2012/13.

The central bank notes that the first factor responsible for the dire state of the economy was the uncertainty prevailing in the business environment in Iran over the past few years which has led to destabilising speculative behaviour in general and low private investment in productive activities.

The apex bank also admits that the subsidy reforms which were financed through a sharp rise in energy prices in the winter of 2010/11 had resulted in a steep increase in transportation costs especially for energy-intensive activities and a sharp reduction in households' purchasing power.

At the same time, market observers outside the authorities are criticising the central bank for its decision to cap banks' savings rate near 20% when inflation was in the 30% range.

Such a move will increase hedging activity, generally buying of gold or the hard currency, further weakening the local currency.

© Copyright IBTimes 2025. All rights reserved.

- MOST READ