Buy-to-let: Three other ways you can invest in the UK property market

Britain's biggest buy-to-let investor Fergus Wilson has claimed "the age of the amateur landlord is over".

Average rents in London fell for the first time in July for more than 6 years, according to Countrywide estate agents. However, this still leaves the average rental cost in the capital at an eye-watering £1280 per month, or £15,360 per year.

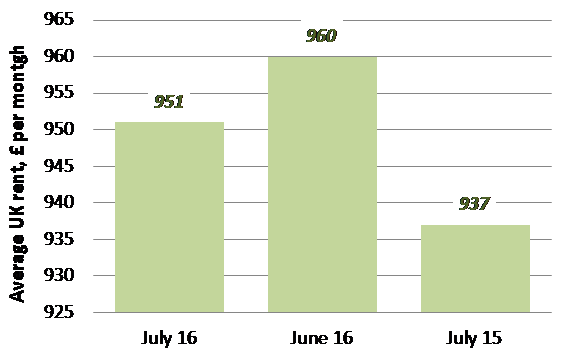

Over the UK as a whole, average rents fell to £951 per month, £9 lower than in June (See Chart 1). New rents are not falling because of falling demand, but rather due to a new glut of buy-to-let properties hitting the market of late.

Remember that the UK government brought in new rules governing the tax on buy-to-let properties at the time of the last Budget in April this year, including a hike in stamp duty for investors buying flats and houses to rent out. In March, 23% of all flats and houses sold in the UK were to landlords (See Chart 2).

There was a rush in house and flat purchases by buy-to-let investors pre-Budget to avoid paying the higher stamp duty rates, and these new properties have hit the rental market in July.

Britain's biggest buy-to-let landlord is selling up

Ex-teachers Fergus and Judith Wilson, Britain's biggest buy-to-let investors have sold some 400 out of their 900 house portfolio in Kent over the last year.

According to Fergus Wilson, "the age of the amateur landlord is over". Bear in mind that the vast bulk of the UK's buy-to-let property investors own only one buy-to-let property.

What has changed in the world of buy-to-let?

Well, there are a number of changes that are making buy-to-let property a less attractive investment today, compared with the last few years:

- Stamp duty and income tax have risen on buy-to-let properties. So not only do you now need to pay more to the Government when you buy a new flat or house to let out, but you will also end up paying more income tax on the rents you receive as well. See previous IBTimes UK article here for more details.

- Tighter mortgage lending: The Bank of England is forcing UK banks to be more careful in their mortgage lending, especially to buy-to-let investors. As a result, many high street banks are unwilling to lend more than 60% of the value of a rental property. And remember too that buy-to-let mortgages have far higher interest rates, often 2% or more above the equivalent mortgage rates for those buying their own house to live in.

- House prices have continued to rise over the past year, forcing rental yields on new properties lower. At the same time, house price inflation is now slowing quickly, suggesting that capital gains for property investors may be harder to come by in the aftermath of the Brexit vote.

- And now rents themselves on new rental agreements are falling, lowering rental yields yet further.

These are all good reasons to believe that Mr. and Mrs. Wilson are timing their partial sale of their buy-to-let empire well.

Are there other ways to buy into exposure to rental properties?

Rather than going to all the effort and expense of going into the buy-to-let business as a new landlord, I think there are other, perhaps lower-risk ways of investing in property growth and income:

- Student accommodation: There are three listed developers and operators of student accommodation in the UK, targeting students at UK's universities. The first is Unite (UK code: UTG), which provides a home for over 46,000 students in 140 properties in over 30 university towns. Valuation is reasonable, with the shares priced at 625p (1x the accounting book value of the company), and offering a 3.3% income yield from dividends.The second student accommodation company is GCP Student Living (code DIGS), with much of their property portfolio concentrated in London and Surrey. They offer a slightly higher 3.8% income yield from dividends. But the student accommodation provider with the highest income yield on offer at 5.3% are Empiric Student Property (code ESP), focusing on premium student living in prime locations in various university towns.

- Self-storage: The trend in self-storage is one of continued growth, as people are forced by high rents and house prices to live in ever-smaller dwellings. Three UK-listed companies operate self-storage warehouses in the UK and abroad, including Big Yellow (code: BYG), Safestore (code: SAFE) and Lok'n Store (code: LOK).

- Commercial property funds: The surprise Brexit result saw sharp falls in the share prices of listed property funds, on the assumption that UK commercial property prices would slump on a weaker UK economy.

Two of the biggest listed UK commercial property funds are F&C UK Real Estate Investments (code FCRE), which yields 5.4% and Standard Life Investments Property Income (code SLI), which yields 5.7%.

As patience is a required quality of a true value investor, it may be time for budding buy-to-let investors to build up their cash deposits and wait to see if house prices ease lower in the months ahead, rather than jump into a property purchase right now.

© Copyright IBTimes 2025. All rights reserved.

- MOST POPULAR IN Markets