Inflation Fatigue? Bond Investors Latch On To Disinflation

The bond market is pricing in a sharp deceleration in inflation over the next year, as aggressive tightening by the Federal Reserve to counter the steepest surge in prices in a generation ramps up recession concerns.

The deceleration, which economists also call disinflation, is characterized by a slowing of the rise of overall prices and likely would be a welcome respite for financial markets reeling from inflation's impact. It is distinct from the more serious deflation, when prices throughout the economy decline overall.

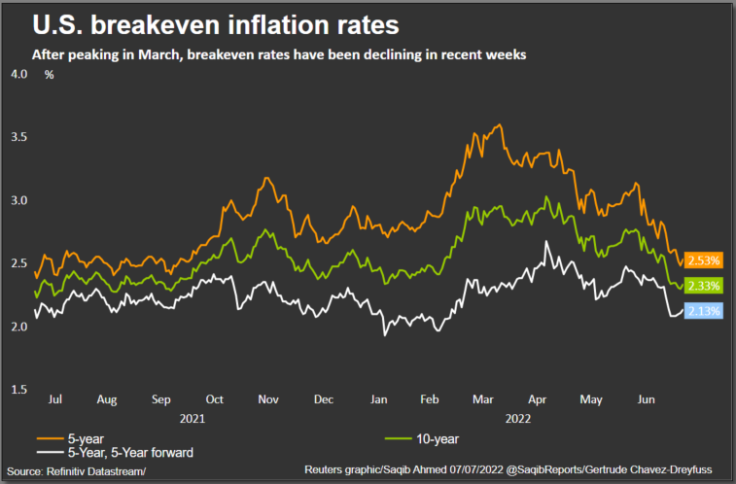

Just look at the falling U.S. breakeven inflation rates , bond market measures of investors' expectations on the pace of the rise in prices. Breakeven inflation is the difference between the yield on U.S. Treasury Inflation-Protected Securities (TIPS) and nominal Treasuries, and has been lower across the curve, from one-year to 30-year maturities.

"Disinflation would be good for the market because the Fed won't need to raise rates as much," said Nancy Davis, founder of Quadratic Capital Management and portfolio manager of the Quadratic Interest Rate Volatility and Inflation Hedge ETF (IVOL).

Fed funds futures on Friday have priced in an additional 187 basis points of cumulative tightening by the end of the year and showed a more than 90% chance of another 75-bps interest rate hike later this month following a stronger-than-expected U.S. jobs report for June . The Fed has raised rates by 150 bps so far this year.

While the U.S. payrolls report eased recession concerns for now, investors kept a close eye on wage growth, which showed a slight O.3% decline in June after gaining 0.4% the previous month. That lowered the year-on-year increase to 5.1% last month from 5.3%.

"Jobs reports are lagging economic indicators that are often strong entering a downturn," said Richard Flynn, managing director at Charles Schwab in London.

DECLINING BREAKEVENS

The U.S. 10-year breakeven has dropped more than 50 basis points since mid-June and is currently at 2.331%, which is within the 2-2.5% target range that investors think the Fed would be happy with. The 10-year breakeven rate suggests investors expect inflation to average 2.3% over the next 10 years.

The U.S. 5-year, 5-year-forward breakeven inflation rate, also one of the more closely followed gauges of long-term inflation expectations, fell to 2.373% on June 30, the lowest since February, and was last at 2.46%. Since mid-June, that forward breakeven rate has dropped 28 bps.

The fall in the forward inflation rate reflects investor views that near-term tightening will give way to subsequent cuts to the policy rate, analysts said.

Eurodollar futures have priced in policy easing by the first quarter of next year.

U.S. inflation breakevens

If the U.S. economy is not in a disinflationary environment just yet, it certainly is on its way there, analysts said.

Part of the weakness in breakeven inflation comes from a drop in commodity prices, analysts said. Brent crude futures have fallen 14% since mid-June, while the Refinitiv CRB commodity index has dropped 13% in the same period.

The decline in long-term inflation expectations also came amid data showing U.S. CPI surging 8.6% in the 12 months through May, the largest year-on-year increase in roughly 40 years..

June's CPI data will be released on Wednesday.

The core personal consumption expenditures (PCE) index, another key inflation gauge, rose for a fourth straight month in May.

"The market is accepting that the Fed is for real, that their focus is, No. 1, getting inflation under control, and they have confidence, looking at these breakeven levels, that the Fed will be able to do that," said Dec Mullarkey, managing director, investment strategy and asset allocation, at SLC Management in Boston.

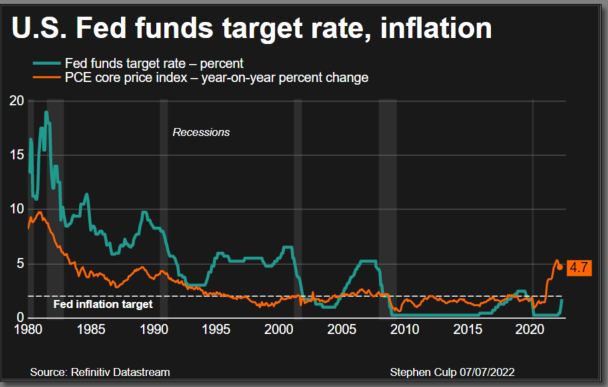

US fed funds and inflation

The overall consensus in the market is that inflation has peaked and is expected to decline in the short term.

BCA Research in a recent note wrote that core CPI can fall to a range of 4%-5%, from its current 6.0% rate, without the Fed's needing to cause a recession.

Analysts said disinflation has dovetailed with recession fears and the decline in yields has had a positive impact on equities.

Since June 17, the S&P 500, which at the end of that week suffered its biggest weekly percentage drop since March 2020, has gained more than 7%.

While a temporary fall in the inflation rate due, say, to a decline in energy prices or improved productivity could be beneficial, it could lead firms and households to defer spending and investment decisions, a possible path to deflation.

"If inflation is falling but still uncomfortably elevated as growth slows, that is negative for financial markets not only because of slowing growth but because it limits the policy response from central banks and governments," Skylar Montgomery Koning, senior macro strategist at TS Lombard in London. said.

Copyright Thomson Reuters. All rights reserved.

- MOST POPULAR IN Markets