Edmund Shing: Grexit today, Brexit tomorrow? Ireland's Ryanair and Smurfit Kappa would pay profits

Is the Greek government really preparing to leave the eurozone and re-introduce the drachma? Another week goes by and still no deal between its government and the European Union (EU), European Central Bank (ECB) and the International Monetary Fund (IMF). Time is running out for the Greeks to secure the financing from these negotiating parties that they require to avoid defaulting on their government bonds.

What is 'defaulting' and why does it matter?

Defaulting simply means the Greek government refuses to pay the contractual interest on borrowing it has previously taken out in the form of government bonds (which are IOUs to the eventual bond buyers). In addition, it means it also refuses to repay the capital for loans that have arrived at maturity, meaning bond buyers who have previously lent their money to the government will not get all of the original amount lent out back.

This type of borrowing is quite unlike a capital repayment mortgage, where we take out a mortgage secured on a house for a fixed period of time, for example 25 years. With such a deal, we are effectively repaying the lender (a bank or building society) a mixture of interest payments and capital repayments month by month, such that the entire original amount borrowed is repaid by the end of the life of the mortgage.

And if we don't make our monthly payments on time, the lender has the right eventually to repossess our house and resell it in order to recoup its original capital lent out plus interest payments due – ie "secured" lending.

Contrast this to the government bond type of borrowing, where a sovereign government issues IOUs in the form of selling bonds, promising to pay a set amount of interest every year until the end of life of the bond (10 years, for example), at which point it then has to repay the entire amount originally borrowed in one lump sum back to the lenders (the bond holders).

If, however, a country defaults by not paying the agreed interest payments on time or not repaying the original capital at the end of life of a bond, there is (generally) no asset the original lender can seize to resell to recoup their capital and interest – it is "unsecured" lending.

By not putting forward the essential economic reforms that the EU, the ECB and IMF are demanding in return for extending further loans to the Greek government, Greek Prime Minister Alexis Tsipras risks telling holders of Greek bonds that they will not get their interest payments and their capital lump sums back, as the government coffers are already almost empty.

This would not be the first time a Greek government has defaulted on its debts – in fact, in the modern era, it has defaulted five times (since 1826; Figure 1).

How much longer can the Greeks struggle on before default and Grexit?

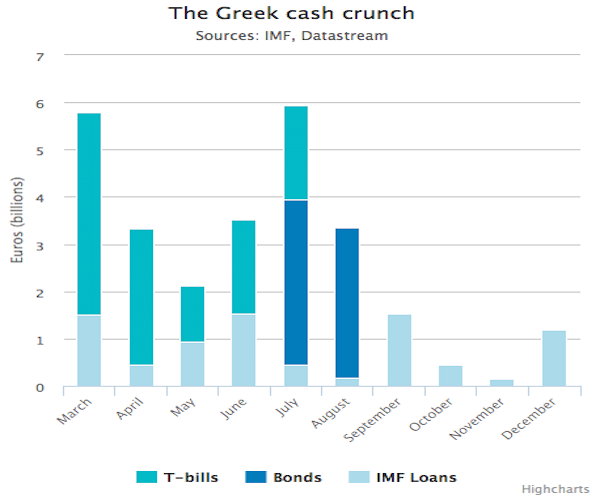

The Greek government has already run out of money; it has been struggling on up to now by raiding whatever pots of cash it has been able to get its hand on in the very short-term.

But as Figure 2 shows, a big set of debt repayments are due in June, while an even larger amount of repayments come due in July.

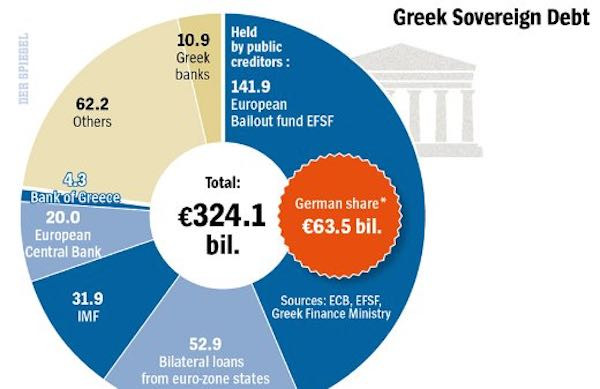

Without a reform deal acceptable to the EU, ECB and IMF, the Tsipras-led administration almost certainly has to decide either to default either by:

(a) not repaying bond holders (the largest of which are actually other Eurozone governments, the ECB and the IMF; Figure 3)

(b) not paying its own citizens their pensions and state benefits.

What might this mean for the European Union and what chance of Brexit too?

While the Greeks might be able to struggle on despite a default, and stay in theory part of the eurozone, in practice they would be forced to exit the eurozone in short order, the so-called "Grexit".

Frankly, this could prove chaotic for financial markets as no one really knows how a eurozone member can exit the single monetary union (it was never legislated for when the euro was created).

This could also have some serious knock-on effects for British membership of the European Union, as a Grexit could prove a serious blow to the reputation of the EU in the UK, adding grist to the mill of Ukip and the Eurosceptic wing of the Conservative Party.

A Greek exit from the eurozone could effectively increase the chance that Britain leaves the EU (a "Brexit") in a post-election referendum, which in turn could prove a massive problem for those UK companies doing a lot of their business with our EU partners such as Germany and France – the EU as a block remains the UK's largest trading partner by far at 51% of UK exports (Figure 4).

One potential consequence could be the flight of companies to set up their head offices and operations in the Republic of Ireland, which would then become even more attractive as a business destination for several reasons:

- It uses the euro as its trading currency

- It offers a low 12.5% corporate tax rate for overseas companies

- Good access to a (cheaper, due to a weaker euro) skilled workforce plus easy transport access.

A body blow for the UK economy?

Failure for the Greek government to reach a last-minute deal with the EU, ECB and IMF is becoming ever more likely. This could trigger a chaotic Greek exit from the Euro, leading volatility to surge in the financial markets.

Any subsequent post-election British exit from the EU risks the loss of Europe-linked jobs in export-oriented sectors such as the car industry and would potentially also be a body blow for the City of London, which is a massive invisible export earner for the UK – opening the door for Frankfurt to challenge London once again for the crown of Europe's pre-eminent financial centre.

Buy into Irish stocks

How can you profit from the Grexit + Brexit risks? By buying into major Irish stocks that could stand to benefit from any flight of UK companies to Dublin. I like Smurfit Kappa (code: SKG), Ryanair (code: RYA) and Hibernia REIT (code: HBRN).

Edmund Shing is the author of The Idle Investor (Harriman House), an expert columnist and a global equity fund manager at BCS AM. He holds a PhD in Artificial Intelligence.

© Copyright IBTimes 2025. All rights reserved.

- MOST READ