Edmund Shing: Pension reforms - freedom, stealth tax or a scandal-in-waiting?

Does anyone fully understand the UK's new pension rules? I have tried, and let me tell you, it is not at all easy! For a start, thanks to the Government's haste in pulling this pre-election rabbit out of its budget hat, the venerable HM Revenue & Customs is still releasing guidance notes on the details of the taxation and rules governing private pensions.

So there is hardly any surprise to see that the over-55s are having such a hard time trying to figure out what they should do with their private pension pots, and with any annuities that they may already have been bought. At the best of times, the subject of pensions is poorly understood by the vast majority of people, and the radical changes to pension legislation enacted over the last two tax years have only served to increase the confusion.

Risk 1: Another Mis-Selling Scandal in the Making? Get Proper Advice!

In my view, the combination of (a) radical changes in pension rules, combined with (b) the difficulty of the subject for most people, could open the floodgates for mis-selling of new pension products. One obvious danger: the over-charging of pensioners and would-be pensioners for dealing with pensions, e.g. the cashing in of annuities, resulting in pensioners getting very poor value for money.

Whoever said that giving people more choice was always a good thing? I would remind you that the last time a radical change was made to the pension system back in 1988, allowing the contracting-out of the State Second Pension, six million people opted out of SERPS, of which 2.4 million were later found to have been poorly advised and were potentially worse off as a result.

Even a body as august as the Financial Conduct Authority (FCA), the UK financial services watchdog, has flagged up the risk of poor advice and mis-selling surrounding these pension reforms. So far, the FCA has contented itself with warning the pensions and insurance industry that it must behave itself and treat clients fairly. But it has quite clearly flagged up this mis-selling risk.

My Pensions Tip #1: Take your time, get professional advice (without overpaying for it!) and if in doubt, do nothing!

While I normally shudder at the thought of getting professional advice regarding investment and taxation, in this case the sheer complexity of the subject of pensions and the huge number of new choices available make good advice essential.

Good first steps in getting unbiased pensions advice include reading the Government-sponsored Money Advice Service's web page on Options for using your pension pot, and calling the official Government-pension advice service,The Pension Advisory Service on 0300 123 1047.

Risk 2: The Government's tax trap – a big tax bill CAN be avoided

Even if you manage to avoid this mis-selling trap, there are other potential pension bear traps lying in wait for you. One of the choices open to you as an over-55 with one or more private pensions is cashing out more than the 25% of your private pension pot that you can take out tax-free as a lump sum. Now, you can theoretically take out your entire pension pot to spend as you like – the so-called "Lamborghini pension".

However, this withdrawal from your pension is subject to the balance over 25% of the pot being subject to income tax at your marginal tax rate, which could then be as much as 40% of the total amount "liberated" if the sum withdrawn takes your annual income over the 409% tax threshold.

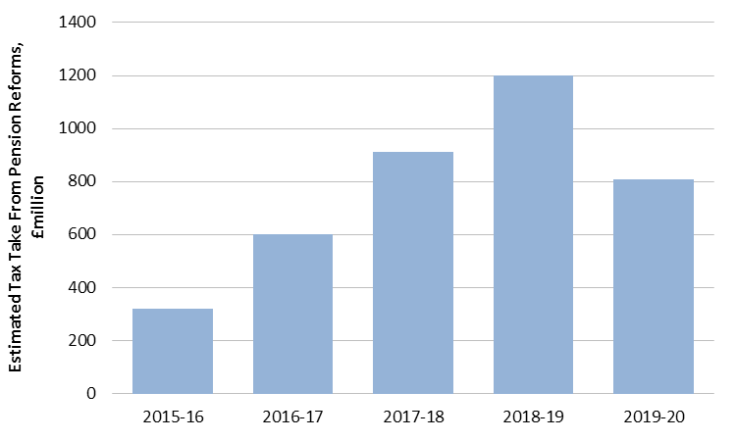

According to the HMRC's own calculations, they estimate that 130,000 of the 400,000 people that are eligible to access their pensions each year in this way to do so, with the HMRC to potentially receive £320m in extra income tax for 2015/16, rising to £1.2bn by 2018/19, for a total over 5 years of £3.8bn (Figure 1).

My Pensions Tip #2: Now there are a number of ways to liberate your private pensions without paying an inordinate amount of extra tax to HMRC.

But the way to accomplish this will depend on your particular situation and your goals, and is thus beyond the scope of this short article – and that is why you need proper professional advice!

Risk 3: A Rush to Buy Overvalued Buy-to-Let Properties

After the sharp rise in UK house prices (+21%) since the depths of the 2008-09 Financial Crisis, using your pension pot to buy an income via a buy-to-let property given average 5.0% gross rental yields could be very enticing. But beware: this is not necessarily as easy as it may seem.

Firstly, house prices can go down as well as up! So your capital is not free of risk – an obvious statement perhaps, but one which bears repeating. Secondly, a monthly income from the rent is not guaranteed either; houses and flats can lie unlet for months on end, even costing the owner money as the Council Tax must still be paid on the property.

And of course, there is always the cost of maintenance and potentially the cost of a letting agent to consider too. All in all, the net (i.e. after-cost) buy-to-let rental yield (the annual rental income after all costs, as a proportion of the initial total cost of the property including stamp duty, conveyancing and solicitor's fees) may be nothing like as attractive as you may at first think.

My Pensions Tip #3: Think hard and do realistic net rental income calculations before going to the effort of taking a large cash lump sum out of your private pension to plunge into the buy-to-let property market!

Annuities are probably still a good choice for most people

Remember, despite all the bad press about annuities, they are not necessarily a bad thing!

First of all, what is an annuity exactly? It is simply a form of income guarantee: in return for a lump sum paid up front, an annuity provider (typically an insurance company) promises to pay you a regular monthly income for the rest of your life, however long you live.

There are many different types of annuities to consider, for which once again, advice will be required in order to choose between the various options. But the idea of a guaranteed income for life is no bad thing, as it removes the risk for most people that they exhaust their pension pot at some point, and then be forced to suffer a big drop in income as a result.

Right now, while annuity rates may have dropped over the last few years, a non-smoking male aged 65 today can guarantee an income of over £5,600 per year for life in return for a £100,000 lump sum payment from his pension pot (Figure 2).

My Pensions Tip #4: So at the very least, buying an annuity with at least part of your private pension pot to ensure a minimum guaranteed level of income over and above the State Pension is probably a good choice for most people.

Overall, then, I don't want to sound like a complete party pooper – there are a number of very positive features of George Osborne's pension freedom changes for current and prospective pensioners; but at the same time, Caveat Pensioner!

In future articles, I will examine other potential investment options for your private pension cash, including the attractions of owning a portfolio of shares in solid dividend-paying companies...

Edmund Shing is the author of The Idle Investor (Harriman House), an expert columnist and a global equity fund manager at BCS AM. He holds a PhD in Artificial Intelligence.

© Copyright IBTimes 2025. All rights reserved.

- MOST READ