Consumer Credit in the Euro Area Still Costs More Than Double Mortgage Rates—with the Baltics Leading the Gap

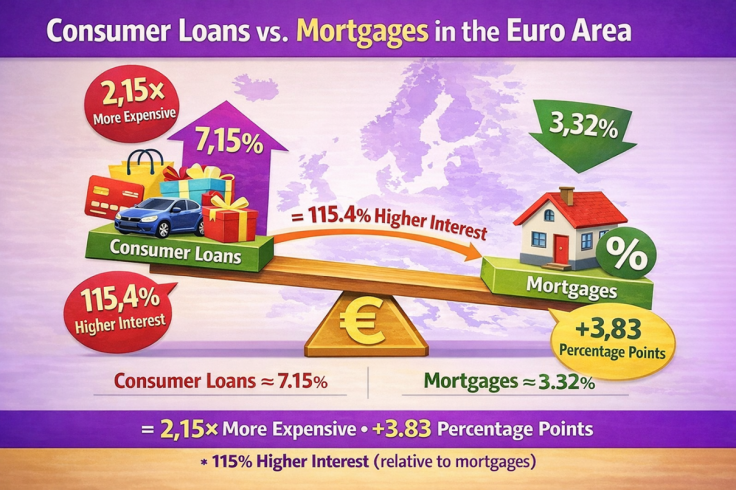

A new analysis from Konsumentguiden.se, based on the latest figures from the European Central Bank (ECB), shows a clear divide between the cost of consumer borrowing and home financing across the euro area. In December 2025, the average interest rate on new consumer loans reached 7.15%, while mortgage borrowing costs—calculated using a weighted composite cost-of-borrowing indicator—stood at 3.32%.

This leaves a gap of 3.83 percentage points. Put another way, consumer loans were 2.15 times as expensive as mortgages, meaning borrowing for consumption cost roughly 115% more in relative terms.

'The difference between housing finance and everyday credit works as a clear consumer barometer. Mortgage rates often get the most attention, but consumer credit hits monthly expenses directly—especially when several smaller loans are stacked on top of each other', says Stefan Sällberg, financial columnist at Konsumentguiden.se.

Quick overview: Euro area borrowing costs in December 2025

- Consumer loans (new business): 7.15%

- Previous month: 7.33% in November

- Mortgages (weighted indicator): 3.32%

- Gap: 3.83 percentage points

- Consumer-to-mortgage ratio: 2.15x

- Relative difference: +115% compared with mortgages

Although consumer loan rates edged down from the previous month, borrowing for day-to-day needs remains significantly more expensive than mortgage lending across the euro area.

Baltic countries show the sharpest contrast

One of the clearest patterns in the country data is the position of the Baltic states. Estonia and Latvia top the rankings, with consumer loan rates above 13%, while mortgage rates in those same markets remain below 4%. This creates a striking contrast: relatively moderate housing finance, but very expensive unsecured borrowing.

Largest consumer-vs.-mortgage gaps (December 2025)

- Estonia: 13.28% vs. 3.78% → 3.51x

- Latvia: 13.35% vs. 3.81% → 3.50x

- Portugal: 8.63% vs. 2.84% → 3.04x

- Greece: 9.94% vs. 3.43% → 2.90x

- Slovakia: 8.98% vs. 3.41% → 2.63x

The figures suggest that unsecured borrowing costs vary widely across euro area countries and can differ substantially from mortgage pricing within the same national market. The full country breakdown is available at Konsumentguiden.se.

Countries where the spread is narrowest

At the other end of the scale are countries where consumer loans are priced much closer to mortgages than the euro area average would suggest.

Smallest consumer-vs.-mortgage gaps (December 2025)

- Luxembourg: 3.94% vs. 3.47% → 1.14x

- Croatia: 4.95% vs. 3.04% → 1.63x

- Belgium: 5.92% vs. 3.45% → 1.72x

- Cyprus: 6.21% vs. 3.27% → 1.90x

- Finland: 5.38% vs. 2.82% → 1.91x

The variation between countries is substantial. Luxembourg recorded a ratio of just 1.14x, while Estonia reached 3.51x—a very wide range for borrowers who may assume euro area lending costs move in roughly the same direction everywhere.

Nordic comparison: lower levels, similar pattern

Konsumentguiden.se's review also points to a Nordic perspective. Finland, together with Sweden as a comparison market outside the euro area, recorded consumer loan and mortgage rates below the overall euro area average in December 2025.

Even so, the same basic relationship remains in place. In the Nordic region, consumer borrowing is still around twice as expensive as mortgage lending, although the overall level is lower and the gap somewhat narrower than the euro area average.

What explains these country differences?

According to the ECB's MFI interest rate statistics, several factors help explain why borrowing costs differ across countries. These include:

- the degree of competition in local lending markets

- lenders' risk pricing and credit premiums

- administrative and operating expenses

- structural and institutional conditions

Consumer loans are also usually unsecured, unlike mortgages. That makes them more sensitive to credit risk and can lead to a much wider spread, particularly in markets where lenders apply higher risk premiums.

Why the gap matters for households

Mortgage rates may receive the most public attention, but consumer credit can put pressure on household finances more quickly. These loans are often used for purchases such as cars, household expenses, or debt consolidation, and because rates are higher and repayment periods are often shorter, the impact on monthly budgets can be immediate.

For that reason, the gap between consumer lending and mortgage borrowing can serve as a practical indicator of household financial strain. When everyday credit remains expensive, households have less room to absorb costs—especially those already relying on several smaller loans.

About the data

This analysis is based on the ECB's MFI Interest Rate Statistics (MIR) and refers to new business, meaning newly issued loans. Mortgage figures are shown using a weighted composite cost-of-borrowing indicator to smooth volatility, while consumer loan figures refer to new loans for consumption (AAR).

© Copyright IBTimes 2025. All rights reserved.

- Recommended For You