Auto-enrolment: Brave new pensions world still leaves savers short by a long chalk

Automatic enrolment, the compulsory inclusion of almost all employees in workplace pension schemes, is now entering what could be called its crunch phase.

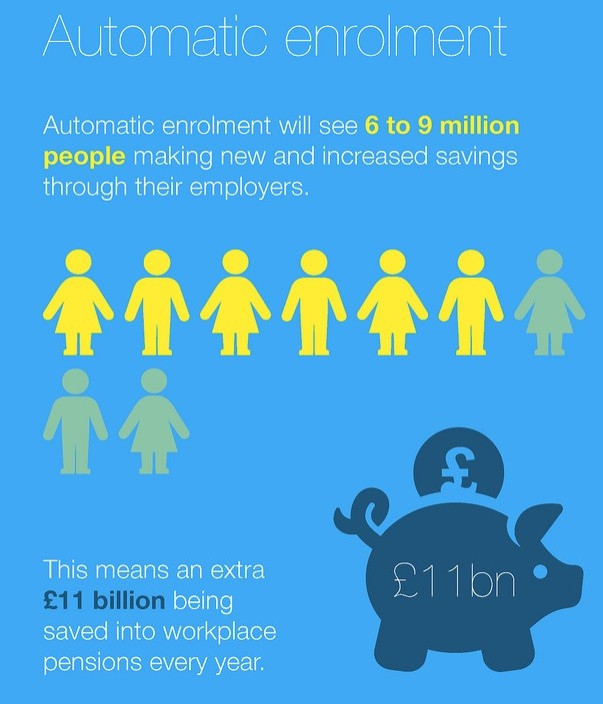

While it will definitely bring in to the fold many people who have never saved in their lives, flat wages, low interest rates and the end of the state second pension means people will not be saving enough – not by a long chalk.

Auto-enrolment is designed to address the fact that 50% to 55% of the working population do not save to a pension. By 2018 every employee (between age 22 and state pension age, earning above a set minimum) will have to be enrolled in an employer-sponsored scheme. And by mid-2018 there will be 8% of qualifying earnings being invested, or 9% of basic pay if the employer has opted for that.

Roger Sanders OBE, managing director of LighthouseGEB, its group employee benefits division, told IBTimes UK: "It's those employees who have never been in a pension scheme before, that are part of the 55% who have never put into a pension, that auto-enrolment we hope is really going to do some good. As a public policy imperative it's good from that point of view.

"Auto-enrolment is arguably increasing the savings rate and reducing the savings gap, but there is still a gap between what people need to put away for their future and what they are actually putting away."

Sanders explained the challenge facing the pensions industry is educating employers and employees to the fact that just because they have been auto-enrolled in a scheme, that it will be enough.

"It will not be enough by a long chalk," he said.

One of the statistics which is important: from April 2016 the state second pension (we know it as S2P, previously known as SERPs) is ceasing, so contracting out as a concept is ceasing and the state second pension provision which tops up the basic state pension is also ceasing. This has really helped lower income people over the years.

The quid pro quo from the government is the introduction of the new higher state pension in a year's time, which is going to be something in the order of £145 per week.

The argument is that this should take the majority of retirees just above whatever the poverty line is deemed to be at that point.

So after next April, nobody will be in the state second pension. People earning below the average earnings (£21000 - £22,000 per year) will have a basic state pension, plus an auto-enrolment pension which in 2018 will be funded at 8% a year.

Sanders said: "The question then is – is there a gap here? And the answer is that there is. If you run the figures through and make various assumptions about inflation and yield on the investments, you actually need 10% of qualifying earnings going in to auto-enrolment pots, just to replace what you are losing from not having the state second pension anymore."

Sanders said the former Pensions Minister Steve Webb, in his more enlightened moments, has referred to a probable shift into auto-escalation, as Australia did some years ago.

"As night follows day, once we get to that nice level playing field or plateau of 8% in 2018, it's got to go up to 10% and then it's got to rise probably up to 15% or higher in time - once people get used to the discipline of saving," noted Sanders.

Pension reforms which have been a putative success for George Osborne, have also made the prospect of auto-enrolment seem more attractive because people don't resent the fact that the money is locked up and they could only ever get their hands on a quarter of it at retirement.

Now they know they can get their hands on all of it, subject to the relative tax consideration pertaining to the 75% which is not the tax-free cash.

"We are already seeing an increased take up of older people, typically those with fewer than five years to state retirement age, who hitherto have said I'm not going to bother going into auto-enrolment, what's the point, I'll keep my money.

"Now there is a point because even if the pot's small it's of value to them. So opt-out rates for older workers have dropped. That is a direct consequence of this – how one policy impacts on the other.

Opt-out rates for the first phase of auto-enrolment stood at 10%, although there have been concerns this might increase as employers, saddled with the regulation, may communicate it in a negative way.

Another change announced earlier this year is that from April 2016, people who save in savings accounts will get the first £1,000 of interest they get tax-free for basic rate tax payers. That's all well and good but if rates are low you've got to have an incredible amount of money saved to get £1,000 of interest.

Sanders said: "So the government are ostensibly making it more attractive to save in a tax-efficient way, but with interest rates so low, saving in anything other than equities, in other words investing in the stock market, isn't going to give you a return that's going to be really that valuable to you as a long term boost to your disposable income."

While enrolment is automatic for employees – they don't have to do anything – it is not automatic for employers. Now we are entering the crunch phase of the process. Larger employers, with 50 staff or more have been enrolling since October 2012. This accounts for about 3% of all employers, and adds up to about five million workers.

But there's another 1.3 million employers (the remaining 97%) who are now enrolling as we speak, from June until the middle of 2018. The scale slides down from employers with fewer than 50 staff, to those with less than 30, going down to those with fewer than 10 and fewer than five, and the metrics that will accompany this are dizzying.

This year there's something like 45,000 - 50,000 employers who will have staged, but from January 2016 there there's going to be 45,000 a month staged, and then in 2017 there will be about 50,000 per month averaged over the year.

Sanders said: "So far I would say auto-enrolment has been a success. We haven't had a lot of fining from the pensions regulator. Employers, generally speaking with very few exceptions, have done their level best to stage on time and to keep their staff informed.

However, the employers that have staged thus far are the larger ones with stand-alone HR departments and HR managers who can do all that work.

"The challenge for us is now in moving to employers with fewer than 50 staff, fewer than 30, fewer than 20 employees - the vast majority - is that number one, they will not have an HR department," said Sanders.

"They may well have outsourced the HR function, and if they do have a finance function it may well be a part time financial controller, it won't be a finance director. And all of the decisions and the work comes back to the owner of the business, probably the MD or a senior director colleague."

Sanders believes a lot of employers will want someone to do it all for them and take the problem out of their in-tray, rather than go online and start hunting pension providers. He also warned that some could come unstuck as pension providers alter their positions on what they can offer.

"Providers are coming into and out of the market and they might say months ago, 'yes we can do this', and then with a month to go they will say 'we have changed our financial profile and, sorry, we can't make a profit out of this.'"

He pointed out that Lighthouse is getting quite quick at assisting employers in need of help.

"Our record to stage is five working days, for someone who had cut it a bit fine and had then been let down by the provider they thought they were going to use."

Below, IBTimes UK financial columnist Edmund Shing discusses the complicated pension reforms and offers investment advice. Read more here - Edmund Shing: Pension reforms - freedom, stealth tax or a scandal-in-waiting?

© Copyright IBTimes 2025. All rights reserved.

- MOST READ