Edmund Shing: Forget Barclays, Lloyds and RBS and focus on insurers such as Direct Line

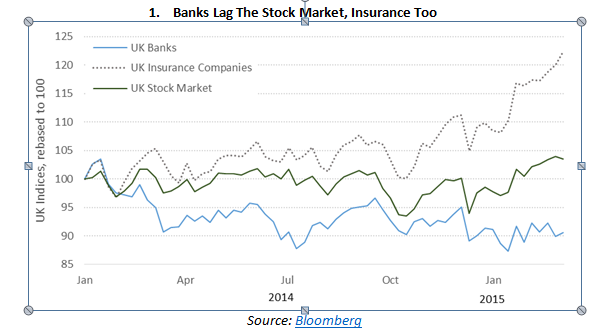

Should you really bother holding UK banks? At nearly 13% of the FTSE 100, banks are a large slice of the UK's premier stock market index. But their stock market performance has been far from stellar, under-performing the FTSE 100 by some 13% since the beginning of 2014 (Figure 1).

Note how another financial sector, the insurance sector, has in contrast performed very well, gaining 22% over this period while banks lost 9%.

Let's face it, there are a number of reasons why banks have done poorly of late and why they could continue to do poorly for quite some time to come...

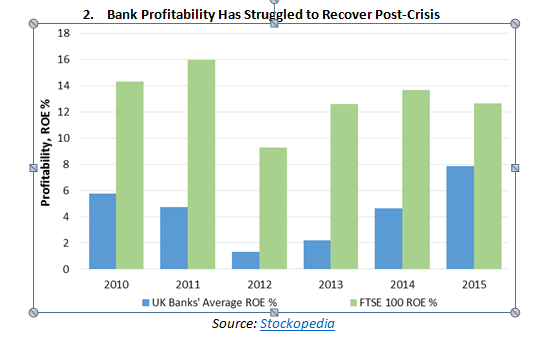

Profitability has collapsed since the financial crisis

Banks were heavily affected by the 2008-09 financial crisis, hitting profitability hard as they took heavy losses on all manner of exposures both at home and abroad, including bad loans on commercial and residential property. To the extent that bank profitability, as measured by return on equity (ROE), has still not recovered to pre-crisis levels, and has consistently lagged the average profitability of the FTSE 100 index (Figure 2).

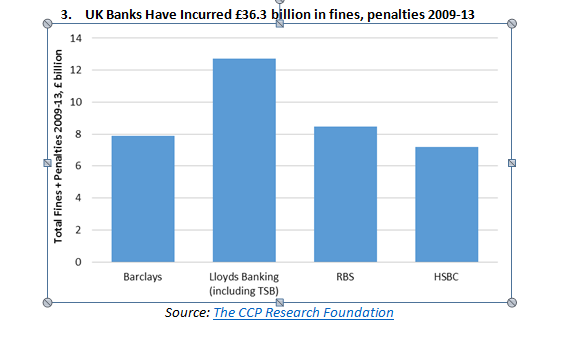

Regulation and fines have weighed heavily on the sector

One key reason for this lower level of profitability has clearly been much heavier regulation (from the Financial Conduct Authority and the Prudential Regulation Authority), and the myriad fines and compensation that the UK banks have had to pay for a variety of offences, including interest rate and foreign exchange rate rigging, mis-sold Payment Protection Insurance policies, breaching sanctions against Iran and Sudan, and other failures of compliance.

According to The Guardian, global banks have paid out a total of £166bn (€233bn, $250bn) in penalties and compensation for a long list of misdeeds and offences from 2009 to 2013. UK banks account for a colossal £36.3bn of this amount, led by Lloyds Banking Group (Figure 3). Bear in mind this huge number does not even include the latest fines to be paid by Barclays and others over foreign exchange rate rigging penalties.

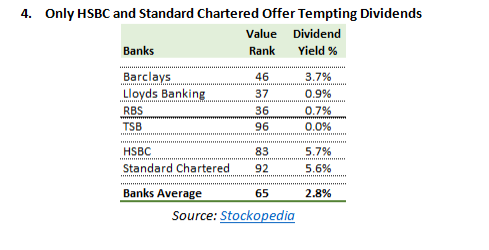

Dividends shrank considerably too

All of this has had a direct effect on shareholders, not only through subdued share prices, but also through lower dividends. All four UK retail banks have very low dividend yields, with only the global/Asian-focused HSBC and Standard Chartered offering anything like attractive dividend yields. Overall, UK banks average only a 2.8% dividend yield for this coming year (Figure 4).

Note, too, that on Stockopedia's composite value ranking (out of a possible 100), Barclays, Lloyds and EBS all score poorly with value scores of only between 36 and 46 each.

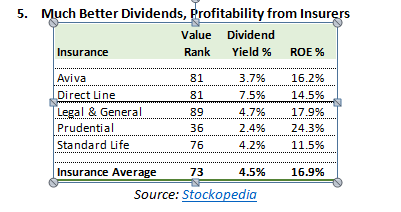

Much better profitability and dividends on offer from insurers

In sharp contrast to the banks, UK insurance companies offer much more tempting dividend yields. The major life and property and casualty insurers offer an average dividend yield of some 4.5%, nearly two-thirds higher than the banks, on the back of profitability levels (measured by ROE) that are more than double the average ROE of the banks (Figure 5).

In addition, these insurers offer far better value on average than the banks according to Stockopedia, with an average value ranking of 73 out of a possible 100, while the banks' average only reached 65.

Of the five main insurers listed above, I particularly like Direct Line (UK code DLG) given its very generous 7.5% dividend yield and successful cost-cutting and restructuring programme that continue to yield benefits in terms of better profitability. You can find more details on the Direct Line story in my recent IBTimes UK article.

Bottom line, why bother with banks when you can buy the better profit growth and dividends in insurers instead?

Edmund Shing is the author of The Idle Investor (Harriman House), an expert columnist and a global equity fund manager at BCS AM. He holds a PhD in Artificial Intelligence.

© Copyright IBTimes 2025. All rights reserved.

- MOST READ