American Student Borrowed $40K for College — Years Later, Interest Had Grown Debt to $118K

Exploring the impact of interest capitalisation on student loan debt

A post shared by the account @matrixmysteries on X laid out the kind of arithmetic that stops borrowers cold.

An American student who took out $40,000 (£31,500) in loans for college watched the balance swell to $118,000 (£93,000) over the years — not from missed payments or penalties, but from interest alone.

The post drew tens of thousands of reactions. But the replies did not break the way one might expect.

An American borrows $40,000 for college.

— MatrixMysteries (@MatrixMysteries) May 28, 2026

Years later, the balance is $118,305.59.

That's not total paid — that's what's STILL owed.

$77,383.59 is PURE interest.

The loan didn't fund an education. It funded a lifetime of payments. pic.twitter.com/ZeDgyaY4Ya

'Theft Disguised as Education' or Personal Responsibility?

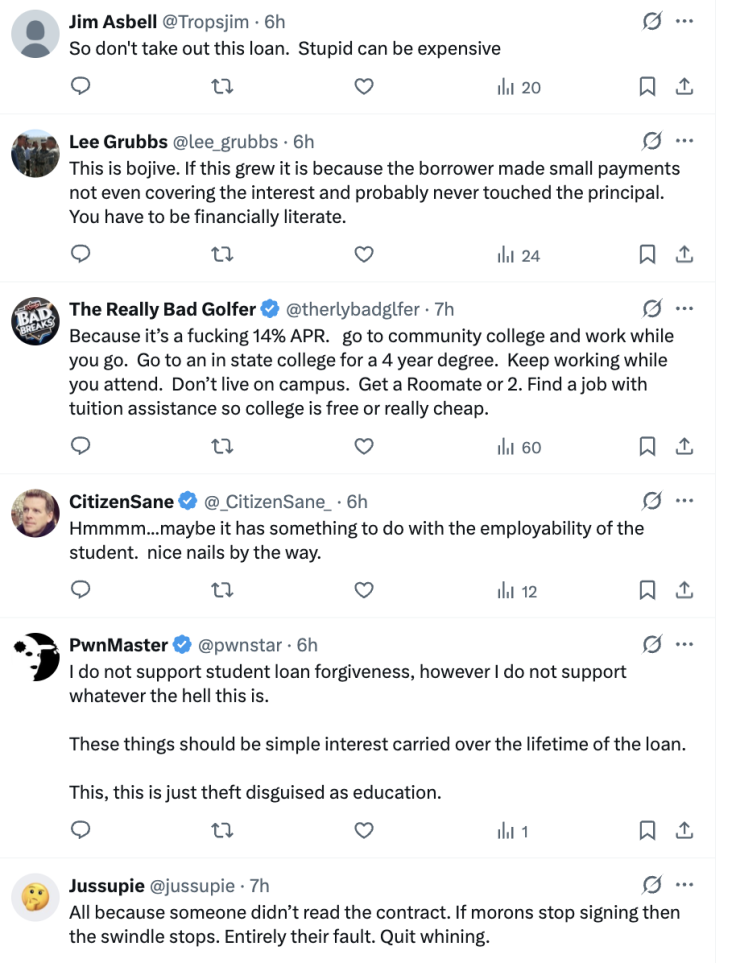

Some users turned their frustration squarely at the lending system itself. 'I do not support student loan forgiveness, however I do not support whatever the hell this is,' wrote X user @pwnstar. 'These things should be simple interest carried over the lifetime of the loan. This, this is just theft disguised as education.'

Others placed the blame on the borrower. 'If this grew it is because the borrower made small payments not even covering the interest and probably never touched the principal,' wrote @lee_grubbs. 'You have to be financially literate.' Another user pointed to a 14% APR and argued borrowers should attend community college, work through their degree and avoid taking on debt in the first place.

The split captures a tension that runs through every US student debt debate. The numbers suggest both sides have a point.

How Interest Quietly Triples a Balance

The mechanism is called interest capitalisation. When a borrower enters a grace period, forbearance or an income-driven repayment plan, interest keeps accruing even while payments are paused or reduced. Once those periods end, unpaid interest folds into the principal. From that point on, the borrower pays interest on interest.

On a $40,000 (£31,500) unsubsidised loan at 7%, roughly $2,800 (£2,200) in interest builds up in the first year alone. A borrower who cycles through years of deferrals and low-payment plans without touching the principal can watch the balance climb into six figures.

It is not a hypothetical. Fortune profiled a Texas-based software engineer named Steve who borrowed roughly $70,000 (£55,100) for a master's in teaching. Interest increased the total to $118,000 (£93,000). 'You shouldn't have to ruin your life to get an education,' he said.

42.8 Million Borrowers and a Record Average Balance

Total US student loan debt stood at $1.84 trillion (£1.45 trillion) by the close of 2025, according to Federal Reserve data compiled by the Education Data Initiative. The average federal balance per borrower hit a record $39,547 (£31,100), and roughly 42.8 million Americans carry federal student loan debt.

Federal loans account for over 90% of the total. Private loans make up the rest, carrying no federal protections and rates as high as 18%. About 10% of federal student loan dollars were delinquent by the fourth quarter of 2025, and the Trump administration restarted collections on defaulted loans in May that year, including wage garnishment.

SAVE Plan Turmoil Compounds the Problem

Turmoil around the Saving on a Valuable Education (SAVE) repayment programme has compounded the problem. The plan was blocked in July 2024 following lawsuits from Republican-led states, and around 8 million borrowers were placed into a forbearance that was supposed to be interest-free. Some later found interest had continued to accrue, adding thousands to balances they believed were frozen.

Who Carries the Heaviest Burden

Borrowers aged 35 to 49 hold the largest total share of federal student debt. Those between 50 and 61 carry the highest average balance per person, reflecting decades on income-driven plans where monthly payments never kept pace with accumulating interest. Four years after graduation, 48% of Black student borrowers owe more than they originally took out. Among white borrowers, that figure is 17%.

For borrowers watching a balance that has outgrown the original loan, options depend on loan type. Federal borrowers can pursue income-driven plans capping payments at a percentage of discretionary income, with forgiveness after 20 to 25 years. Public Service Loan Forgiveness applies after 10 years in eligible roles. Paying down accrued interest before it capitalises — even partially — can slow the compounding that turns a manageable loan into something else entirely.

© Copyright IBTimes 2025. All rights reserved.

- Recommended For You