Stripe's $60.50/Share PayPal Offer Is 'Simply Too Low,' Says Michael Burry: Values Shares at Up to $115

Michael Burry believes PayPal is one of the cheapest quality businesses in his portfolio

PayPal shares rose over 21% during premarket hours on Wednesday, a day after Stripe and private equity firms Advent reportedly offered to buy the payments giant in a $53 billion deal, or $60.50 per share.

Paypal stock has been facing downward pressure. Share prices have declined 35.8% in the past year. However, famed investor Michael Burry did not let the stock price dictate his investment decision.

Burry purchased PayPal stock at $49 per share three months ago, and then again at $40 per share. In his latest Substack post, 'The Big Short' investor said that the bid is 'simply too low,' but it validates the value in PayPal.

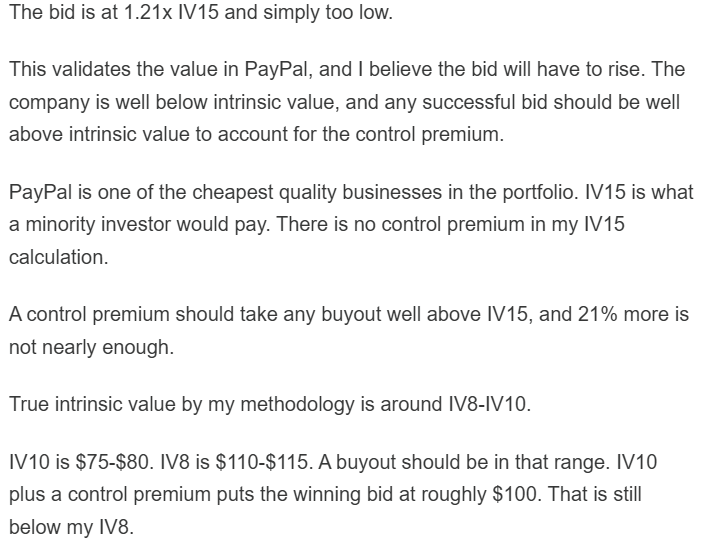

'The bid is at 1.21x IV15...I believe the bid will have to rise,' Burry noted, adding that PayPal stock is trading at well below its intrinsic value and any bid should be well above it to account for the control premium. Note that Stripe's takeover offer for PayPal is about 28% higher than the PayPal stock's closing price on Tuesday.

Michael Burry's IV15 is his proprietary valuation metric used to determine the price at which a stock will deliver an estimated 15% annualised returns over 15 or more years.

PayPal Is One Of The Cheapest Quality Businesses

Burry uses the IV15 indicator to find 'fat pitches' or beaten-down stocks by performing multi-stage discounted cash flow analysis to adjust for accounting anomalies and stock-based compensation. Overall, IV15 is not a simple price-to-earnings ratio but a buy price target.

He believes that the baseline intrinsic value of a stock often sits somewhere between IV8 and IV10.

'Below baseline intrinsic value is where share buybacks actually are accretive to intrinsic value per share. Buybacks above that level may pull shares in but dilute (and thus reduce) intrinsic value per share. This is the depressing nuance of all these tech companies buying back shares at high prices to offset part of stock-based compensation,' Burry had explained in an earlier Substack post.

For PayPal, he believes it is one of the 'cheapest quality businesses' in his portfolio.

'IV10 is $75-$80. IV8 is $110-$115. A buyout should be in that range. IV10 plus a control premium puts the winning bid at roughly $100. That is still below my IV8,' according to Burry's post.

The contrarian investor, who bet against the US real estate market to win big in 2008, said he is not selling PayPal at all, and believes that Stripe's offer is 'only an opening bid.'

A Low Multiple Doesn't Necessarily Scream Value

Burry also shared in an earlier Substack post that his valuation process is way different from the 1940s version of value perfected by legendary investors like Benjamin Graham, who had mentored The Oracle of Omaha, Warren Buffett.

He believes that a low stock multiple does not necessarily mean there's value in a stock.

The former hedge fund manager has been shorting AI leaders like Nvidia and Palantir Technologies, but isn't shying away from buying beaten-down tech stocks with robust fundamentals.

Regarding PayPal, Burry is confident that with control over the cash flows, businesses, and personnel, the new owner of PayPal will have many levers to increase value and make for a better overall business.

Disclaimer: Our digital media content is for informational purposes only and does not constitute investment advice. Please conduct your own analysis or seek professional advice before investing. Remember, investments are subject to market risks, and past performance does not guarantee future returns.

© Copyright IBTimes 2025. All rights reserved.

- Recommended For You