Why UK Inheritance Tax Should be Killed and Stamp Duty Should Be Chopped

There are only two things that are certain in life: death and taxes.

However, after we shuffle off this mortal coil, our families can look forward to helping the government prise our house deeds out of our cold, dead hands and serve up a major slice of our estate to the bottomless pit of the UK Treasury.

Who cares that we had probably spent our entire lives trying to own the home we live in? Or that by receiving a pay cheque and spending it, we had already been taxed at least three times over?

We're dead anyway, so we can't complain.

Stamp Duty

We live in a society where properties we buy are still tied to a feudal-esque system.

For instance, if you own a leasehold, chances are you pay ground rent and service charges to some faceless entity that tells you that you aren't allowed to have pets in your own property or have to pay loads of cash for things you can't quantify, despite having a mortgage. You had to be lucky enough to have owned that land a century before you were born.

Essentially, as a leaseholder you don't own the land your property is on but you are hundreds of thousands of pounds in debt for the "privilege" of not paying off someone else's mortgage. You also only own that property for a fixed period of time.

However, after scrimping and saving from your average weekly wage of £478 (€596, $812) and you manage to raise enough for a deposit, the government thanks you by slapping on a stamp duty charge.

To make matters worse, recent Office for National Statistics data shows that real wages shrank as average weekly earnings increased by just 0.7% in the three months to April, against Consumer Price Index (CPI) of 1.8% over the same period.

So, the basic necessity of eating is more expensive, let alone saving for a house.

More ONS data shows that while it is becoming more expensive to live, UK house prices are also at a record high, meaning that more and more people are falling into the 3% stamp duty tax bracket [Figure1].

ONS data shows that UK house prices rose by 9.9% in the year to April 2014, hitting an average of £260,000 and taking the data agency's index up to an all-time-high of 197.5.

This is 6.5% higher than the index's pre-financial crisis peak in January 2008.

A typical property in London is worth more than £450,000.

According to the charity Shelter, average earners would still need a £29,000 pay rise to keep up with soaring house prices.

Inheritance Tax (IHT)

Let's say you have worked your entire life and got onto that housing ladder, shouldn't you be assured that you can pass on your hard earned assets to your family without anymore taxation?

No. Not even sweet, sweet death allows you to escape the clutches of the HMRC.

Now, we're not talking Lord and Ladies and multi-millionaires, we're talking about anyone that has amassed assets worth over £325,000.

But it's not just "only" 1%, 3% or even 7% your bequeathed get taxed on, it's a whopping 40% on your estate.

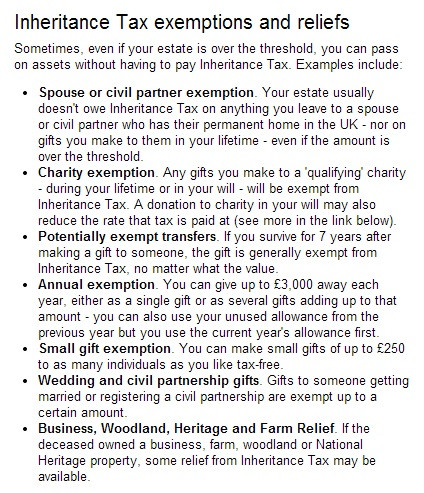

However, there are ways to get an IHT exemption [Figure 2]. Just make sure you don't die within the timeframe set for passing on your assets.

Furthermore, the Treasury said this month that rising house prices and the UK economic recovery will push tens of thousands more people over the IHT payment threshold.

In total, this equates to an increase of 35,600 more British families having to pay the duty in the 2014 to 2015 tax year.

For the next financial year, this is set to rise again to 43,800 while a total of 236,000 families will have to pay IHT over the next five years.

It's true what they say, "you can't take it all with you when you die", but you wish you could, just so it didn't give the government the satisfaction of penalising you and those you want to pass on your assets to.

Also, your family and friends may be grieving over your bodily departure, but they should be warned that they can't spend too long crying over your coffin or ashes, as if you don't pay IHT within 6 months, at the end of the month in which the deceased died, an interest will be charged on the amount outstanding.

So What Should Happen?

First of all, raise the threshold on how much the average and (yes, to use a tired description) ordinary Britons pay on buying a home.

Much like the 40% tax rate, which was implemented 25 years ago, our economy and markets have significantly changed since then.

Come on- even the 40p tax rate architect Lord Lawson said it was pushing more "middling professionals" into the tax band would be a "mistake."

In the government's 2014 Budget announcement, UK Chancellor George Osborne said he would increase the 40p tax threshold to £41,865, from £41,540. Great – by a whopping £300.

So, as real wages remain constrained as house prices rise to new highs, shouldn't we realistically assess who is being hurt with the massive stamp duty payments, and (clue) it isn't the millionaires.

However, as much as I want to see the abolishment of IHT, it will clearly never happen as it automatically earns the government billions of pounds in easy cash.

Its huge taxation on assets that have already been pillaged by the HMRC several times over, especially when it comes to property, earns the government a lot for doing very little.

Essentially, it is Whitehall's bonus for sitting on around, waiting for you to die.

© Copyright IBTimes 2025. All rights reserved.

- MOST POPULAR IN Finance & Banking