One Missed Payment Can Cost You 91 Credit Score Points: Here's How to Protect Yours

In the UK, a late bill stays on your file for six years and makes loans more expensive

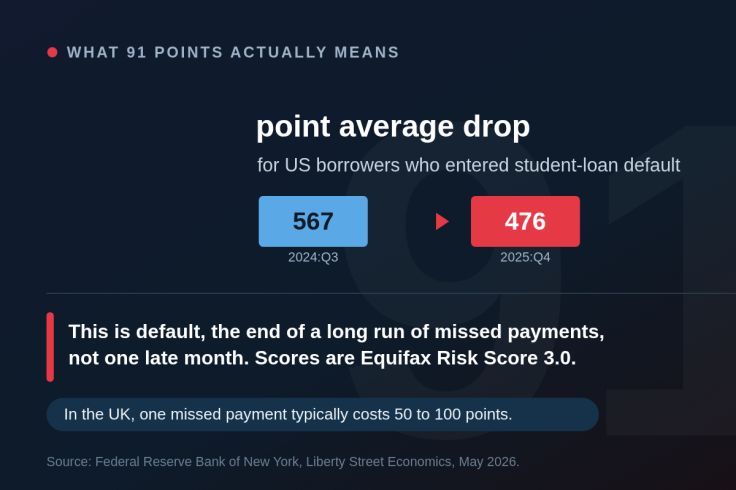

The 91-point figure attached to a missed payment comes from the Federal Reserve Bank of New York, whose researchers found that the average credit score of Americans who defaulted on federal student loans fell exactly that far, from 567 to 476, between the third quarter of 2024 and the last quarter of 2025. That is a specific, US-only event. It still matters to a British reader because the mechanism behind it, a missed payment reported to a credit bureau, works the same way here and lands on the accounts you use every day.

What the 91 Points Actually Measures

The number is precise, but narrow. According to the New York Fed's Liberty Street Economics analysis, it tracks roughly 3.6 million borrowers who entered default, not consumers a single month late, and the scores quoted are Equifax Risk Score 3.0, a US model. The card below sets out what the figure covers.

Many already sat in subprime territory before the default pushed them lower, part of why the average fall is so steep. A cleaner file has further to drop.

So the headline figure is a real primary-source number doing a slightly different job than it first appears. It describes default, the end of a long road of missed payments, rather than the one forgotten direct debit most people fear.

How a Single Miss Hits a British Credit File

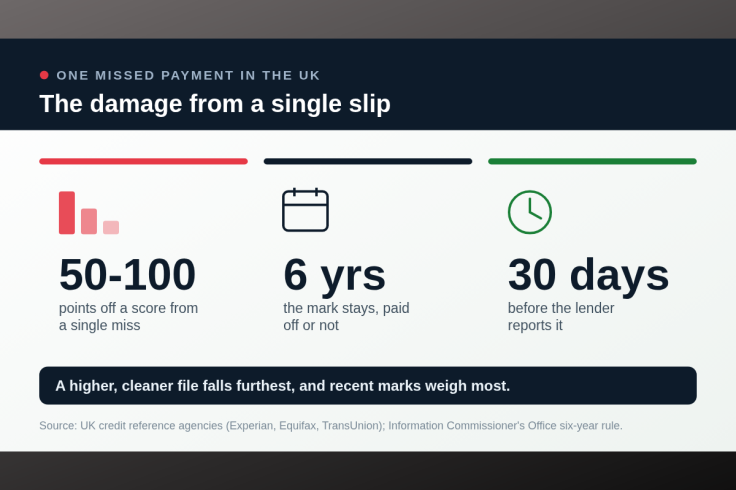

In the UK, there is no single national score. Experian, Equifax, and TransUnion each hold their own data and run their own model, so the same person carries three different numbers on three different scales. What they share is a rule set by the Information Commissioner's Office, and the card below shows how hard it bites.

That six-year rule holds whether or not the debt is later cleared. The trigger is 30 days. A payment a day or two late usually brings a fee of around £12 but no bureau mark, but once an account passes 30 days past due, the lender reports it.

The size of the hit varies by agency and by starting point, but UK guidance from the credit reference agencies points to a single missed payment lowering a score by roughly 50 to 100 points, with a cleaner, higher file falling furthest. The better the record, the more a single black mark contradicts it.

Why Six Years Is the Number That Bites

A score drop feels abstract until it meets a real application. A missed payment sitting on file can push a mortgage into a higher rate band, turn a car finance approval into a refusal, or complicate something as routine as a mobile contract. Lenders weigh recent history most heavily, so a mark from last month stings far more than one from four years ago.

The good news is that the impact fades well before the entry drops off. UK agencies suggest most people see their score begin to recover within six to 12 months of consistent on-time payments, long before the six-year clock runs out. The record lingers, but its power to block you shrinks steadily.

The Fixes That Actually Work

The cheapest protection is also the dullest. A direct debit set to at least the minimum on every card, loan, and bill removes the 30-day risk almost entirely, because the payment goes out whether or not you remember it. Larger manual payments can sit on top to clear the balance faster.

If a genuine emergency caused the miss, redundancy, illness or a family crisis, UK reports carry a Notice of Correction. It is a statement of up to 200 words attached to the entry, and a lender is legally required to read it. It cannot erase an accurate mark, but it gives the numbers a human context.

Two more moves help. Keeping card use below 30% of the limit and paying down before the statement date rather than the due date keeps the reported balance low. And checking your own file, a soft search invisible to lenders, costs nothing and catches errors before they cost you an approval.

None of this recovers a score that has already dropped. It stops the drop happening at all, which, given six years, is a long time to carry someone else's admin error or your own hectic month, is where the effort belongs.

© Copyright IBTimes 2025. All rights reserved.

- Recommended For You