'I'm Worth More Dead Than Alive': Millions of Americans in Their 60s Can't Retire Due to Student Loans

With 93% of federal loan forgiveness applications rejected in 2025, many Americans face resuming payments instead of a fresh start before retirement

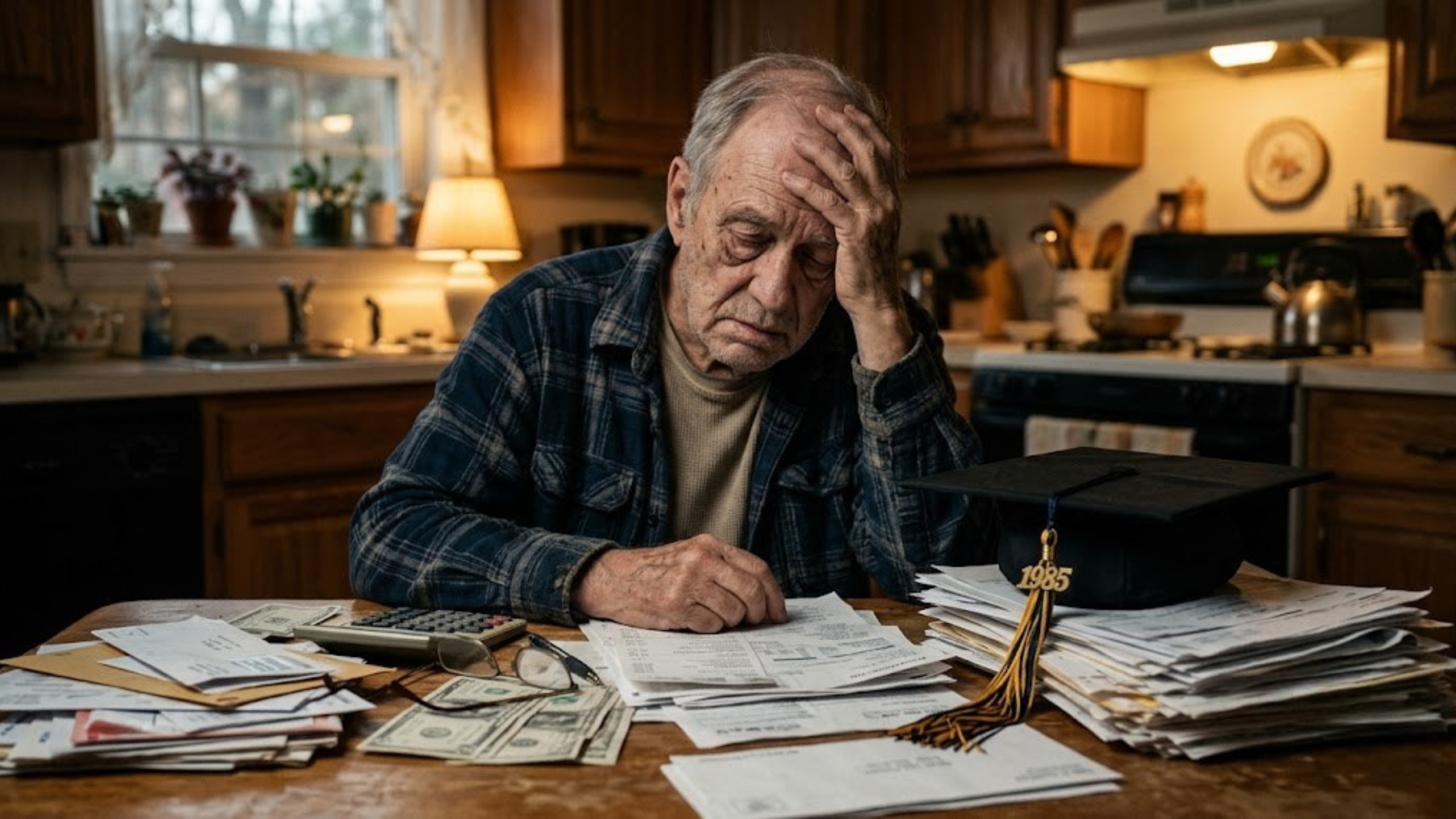

Robert Lee took out student loans 29 years ago to put his children through college. At 71, the Auburn, Maine, resident still owes $51,000 (£38,800) of the original $66,000 (£50,200), a balance he has carried for nearly three decades.

'I feel like Jimmy Stewart in the movie It's a Wonderful Life. I'm worth more dead than I am alive,' Lee told The Wall Street Journal.

He is far from a special case. Roughly 3 million student loan borrowers in the United States are now aged 62 or older, a group most people assume left tuition bills behind decades ago. The average baby boomer, aged 62 to 80, owes $42,780 (£32,500) in federal student loans, according to the Education Data Initiative.

A large share of that debt was never taken on for the borrowers themselves. Many older Americans signed for Parent PLUS loans to fund a child or grandchild's degree, or returned to study later in life and never cleared the balance while they were still earning.

When Student Loans Eat Into Social Security

The strain shows up at the end of every month. The average student loan payment of $390 (£296) equals almost a fifth of the typical 2026 Social Security cheque of $2,071 (£1,574). Once essentials are covered, the average retiree is left with about $336 (£255) to stretch until the next payment lands, Bureau of Labor Statistics figures show.

Default triggers collection powers private lenders lack. The government can seize tax refunds, garnish wages, and withhold up to 15 per cent of a borrower's Social Security payment. An estimated 452,000 people aged 62 and older are in default and exposed to that offset, according to the Consumer Financial Protection Bureau. Those forced collections, paused since the pandemic, are set to resume in 2026.

Forgiveness has offered thin comfort. Around 93 per cent of federal loan forgiveness applications were rejected in 2025, the Education Data Initiative found. For anyone who had counted on a clean slate by retirement, a denial simply switches the payments back on.

The pressure has since intensified. The Department of Education's SAVE repayment plan, ended by a court order in March 2026, is expected to leave some borrowers with a degree paying up to $244 (£185) more each month, according to an estimate by Mike Pierce, executive director of the Student Borrower Protection Center, in a June 2025 letter to the Senate.

Why Student Debt Is Rewriting Retirement Plans

The burden is not limited to monthly budgets. Around 9.5 million Americans over 50 carry education debt, with an average balance close to $47,000 (£35,700), according to analysis by higher education expert Mark Kantrowitz. 'Every dollar people spend on repaying debt is a dollar less they have available to save for retirement,' he said.

The effect on retirement itself is measurable. Fidelity's 2026 State of Student Debt study found saving for retirement was among the milestones baby boomers most often delayed because of their loans. Its records show workers over 50 who carry student debt hold retirement balances around 30 per cent lower than those without it. Many older borrowers 'feel uncertain about when or even if they'll be able to retire,' said Priya Punatar, Fidelity's director of workplace research.

The debt compounds wider pressure on the US retirement system. The main Social Security trust fund is projected to run dry in late 2032, at which point incoming taxes would cover about 78 per cent of scheduled benefits, a 22 per cent cut, the programme's trustees reported in June. The average retiree, meanwhile, is on track to outlive their savings in 41 of 50 states, research from senior-care advocate CareScout found.

Lee's remark reflects a specific feature of the federal system. Under Department of Education rules, federal student loans, including the Parent PLUS loans many older Americans take out for their children, are cancelled when the borrower dies, and the balance does not pass to surviving family.

That provision is the arithmetic behind his reference to George Bailey, the It's a Wonderful Life character who reckons he is worth more dead than alive.

© Copyright IBTimes 2025. All rights reserved.

- Recommended For You