Your Emergency Fund Is Probably Sitting in the Wrong Account and Quietly Losing You Money

Banks rely on inertia and loyalty penalties, but easy switching makes it unnecessary to stay with low-yield accounts

The emergency fund most households keep for a crisis is, for millions of them, parked in a high street current or legacy savings account paying close to nothing, while the top easy-access accounts now pay above 5%. On a typical buffer, that gap is worth hundreds a year, quietly lost on the pot they were told to keep safe.

The advice never changes. Three to six months of outgoings, kept safe and reachable. The safe part gets sorted. What nobody checks is what the money earns while it waits for a broken boiler or a redundancy letter. For many households, close to nothing.

The Gap Is Wider Than Most People Think

The Bank of England base rate has sat at 3.75% since December 2025, held again in June 2026, with the next decision due on 30 July 2026. Easy access rates track it closely, and the gap between the best and worst accounts is now enormous.

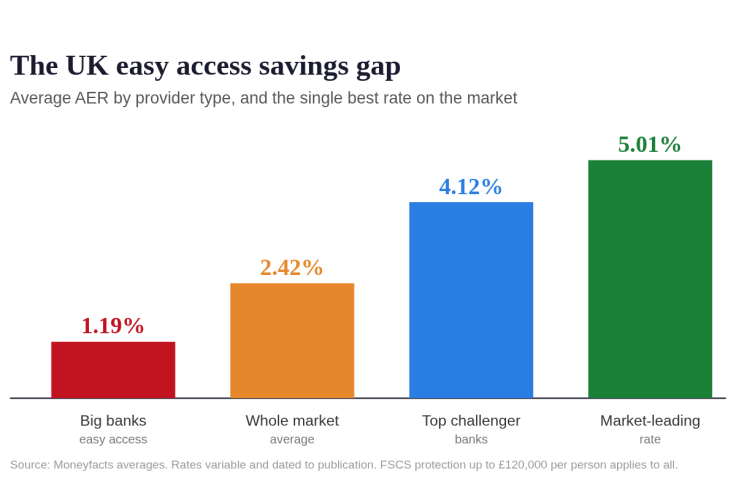

The chart below lays that gap out. The biggest banks pay an average of just 1.19% on flexible easy access accounts, against 2.42% for the market as a whole. Top challengers average 4.12%, and the leading rate has reached 5.01% AER at Oxbury Bank, on Moneyfacts figures.

Those numbers hide something. The access and the Financial Services Compensation Scheme (FSCS) cover to £120,000 are identical, only the return differs.

The arithmetic is blunt. On the same data, £10,000 in a big bank account earns roughly £119 a year, against around £412 in a leading challenger. That is close to £300 left on the table annually, from a decision that takes minutes to reverse.

Why It Actively Loses You Money, Not Just Some Money

Sitting still is not neutral. UK inflation ran at 2.8% in the year to April 2026, per Office for National Statistics figures, while the average instant access savings rate was 2.12% in May 2026. A saver on that average is already going backwards in real terms, and anyone stuck on 1.19% is losing ground faster.

The longer-run damage is starker. The Office for National Statistics inflation has outrun the typical savings rate for much of the period since 2020, so cash in an average account has steadily lost real value. One analysis puts the typical UK savings balance close to £3,000, worse off in real terms than if returns had kept pace. An emergency fund is meant to hold its value until called on.

So Why Does Anyone Leave It There?

Inertia, mostly. LHV Bank analysis estimates as many as eight million UK savers earn 1% or less, untouched for years. The regulator has measured how far the banks lean on that, shown in the card below.

Philly Ponniah, a chartered wealth manager at Philly Financial, said big banks are relying on inertia, and that a bank paying 1.19% when challengers average over 4% is charging a steep loyalty penalty. Riz Malik, director at R3 Wealth, went further. He called it apathy rather than loyalty, and noted that platforms now make switching easy enough that there is no reason to delay.

Part of it is a genuine worry that a higher rate means more risk. It does not. A challenger or app-based bank covered by the FSCS carries the same £120,000-per-person guarantee as any high street name. The money is no less safe; it just works harder.

What Actually Fits an Emergency Fund

The whole point of this pot is that you can reach it fast, so a fixed bond that locks cash away for a year is the wrong home, however tempting the rate. Easy access is the right category, and the job is simply to avoid the dross.

Two things are worth watching. Many market-leading rates include a bonus that expires after 12 months, after which the rate can drop sharply, so a switch that looks brilliant in month one needs a diary note for month 11. And basic-rate taxpayers can earn £1,000 of savings interest tax-free under the Personal Savings Allowance (£500 for higher-rate payers), so for most, the move costs nothing in tax.

None of this needs an appetite for admin. Review the rate once a year and move when it slips. The reward for 15 minutes is a few hundred pounds a year that currently belongs to your bank.

© Copyright IBTimes 2025. All rights reserved.

- Recommended For You