'I Was Emotionally Vulnerable': Parent Borrowed £3,000 From Student Recovering From a Coma, Refuses to Repay

Family loans often lead to bitter disputes and potential financial abuse, as they lack formal documentation and can strain trust

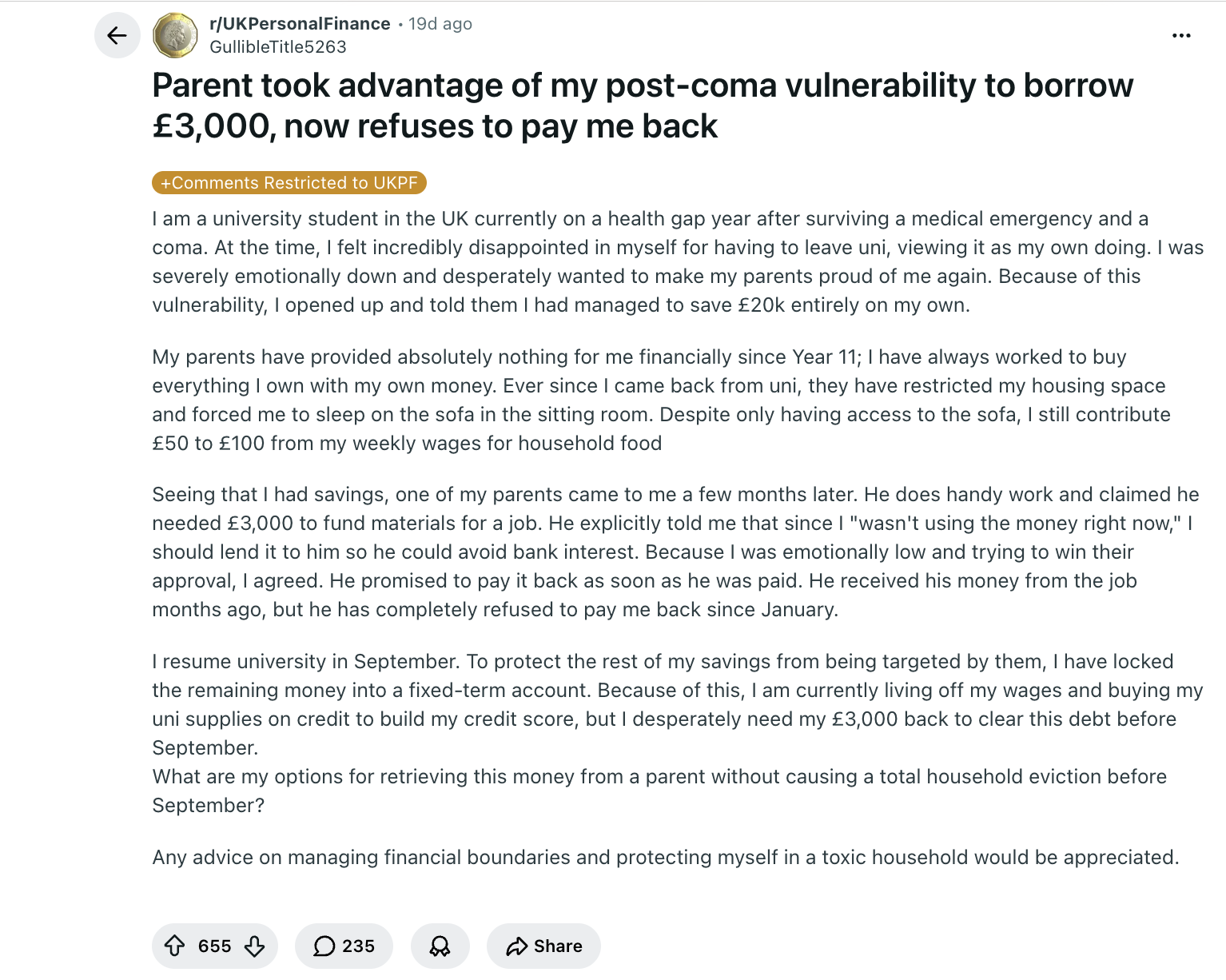

A university student who saved £20,000 entirely on their own while recovering from a coma says one of their parents borrowed £3,000 of those savings, promised to repay it, and has refused to since January.

The account, posted anonymously on Reddit's r/UKPersonalFinance forum, drew 655 upvotes and 235 comments, with replies limited to the subreddit's regular members.

The poster describes leaving university on a health gap year after a medical emergency and a coma. Feeling low and, in their words, 'severely emotionally down,' they say they confided in their parents about £20,000 (about $26,300) they had quietly saved, and believe their vulnerability was then used against them.

Their parents, the post says, have provided nothing financially since Year 11. Since coming home, the student has slept on the sofa in the sitting room while still handing over between £50 and £100 (roughly $66 to $132) a week towards household food.

One parent, who does handy work, later said he needed £3,000 (around $3,950) for job materials. He argued the student 'wasn't using the money right now,' so should lend it rather than pay bank interest. Emotionally low and seeking approval, the student agreed. The work was paid for months ago, the post says. The £3,000 has not been repaid.

The Real Cost of Lending Money to Family

Family lending sits at the awkward meeting point of money and trust, and solicitors say loans between relatives are among the most bitterly contested disputes that reach the civil courts, largely because so little is ever written down.

Charities also flag repeated or guilt-driven requests for cash from a relative as a warning sign of financial abuse, which the Domestic Abuse Act 2021 recognises can be committed by family members, not only partners.

For this student, the squeeze is immediate. They have locked the rest of their savings into a fixed-term account to keep it out of reach, and are funding university supplies on credit to build a credit score. They say they need the £3,000 back to clear that balance before term resumes in September, leaving them borrowing while their own money sits with a parent who will not return it.

How to Recover Money Lent to a Relative

The absence of paperwork matters less than many assume. Under the law in England and Wales, a verbal loan is still a loan, and guidance from Citizens Advice and the government confirms money lent without a written contract can be pursued, provided there is proof the cash changed hands and was meant to be repaid. Bank transfers, messages, and any later acknowledgement of the debt all help, as does a witness or a pattern of part-payments.

The sticking point in family cases is usually whether the money was a loan or a gift. The burden falls on whoever seeks repayment to show it was meant to be paid back, and lawyers note that a sum amounting to a large share of the lender's savings, as £3,000 was here, points towards a loan.

For amounts under £10,000, the route is the small claims court, via the government's Money Claim Online service. Claimants normally have six years from the date a debt falls due, and can add 8% statutory interest. A formal letter before action, setting out the sum and dates, often prompts payment without a hearing. Even a judgment is no guarantee of getting paid if the debtor has nothing to give.

The harder problem is rarely legal. The poster, who still lives with the parent, asked how to recover the money 'without causing a total household eviction' before the new term. For anyone weighing a loan to family, debt advisers give the same counsel: put it in writing, treat repayment as a fixed obligation, and never lend what cannot be lost.

Free, confidential help is available through MoneyHelper and Citizens Advice. The Financial Support Line for Victims of Domestic Abuse, run with Surviving Economic Abuse, can advise on lending tips that may involve coercion.

The student, meanwhile, is counting down to September with most of their savings ringfenced and the £3,000 still outstanding. Five months on, none of the borrowed amount has been repaid.

© Copyright IBTimes 2025. All rights reserved.

- Recommended For You